This article appeared on Kamloops This Week‘s website on January 4th, 2016 and was written by Cam Fortems.

Valleyview and Barnhartvale led city neighbourhoods in a 2015 assessment marked by continued moderate growth for Kamloops and the region.

Homeowners will tear open their assessment letters arriving in the mail this week — or check online — to find values in the range of minus five per cent to plus 10 per cent. Most neighbourhoods saw property values increase in the range of two or three per cent.

“For the most part, values are fairly constant,” said area assessor Graham Held. “Graphically. you can see the vast majority are in the zero to five per cent range [of increase].”

The City of Kamloops uses the calculations as part its annual tax assessment.

The city’s revenue manager, Parissa Bhullar, said a precise average is not yet available. That average will determine whether property owners will get a break or pay higher property taxes in 2016.

On a neighbourhood basis, Barnhartvale homeowners saw the biggest average increase — at $24,000, or about 6.5 per cent. That compares to lower increases in Juniper Ridge, Westmount and Batchelor Heights, where values are up a half per cent or less.

Values are calculated as of July 1, 2015.

The city also saw about $382 million in new construction for the period between July 2014 and July 2015. Held said the higher volume of sales recorded this year helps with valuations. “Sales values were strong, which is good for us because everything is based on sales,” he said.

Held said property owners who believe there is an error or that their values are misrepresented should call B.C. Assessment Authority for a potential correction or to book a time for an appeal with the property assessment review panel.

The deadline to file an appeal is Feb. 1.

Based on moderate increases, Held said call volumes to the office, as well as appeals, are expected to be down.

Across the region, Chase and Sun Peaks saw the highest average increases — as much as 15 per cent — with Logan Lake and the North Thompson among the lowest.

An Active Real Estate Market

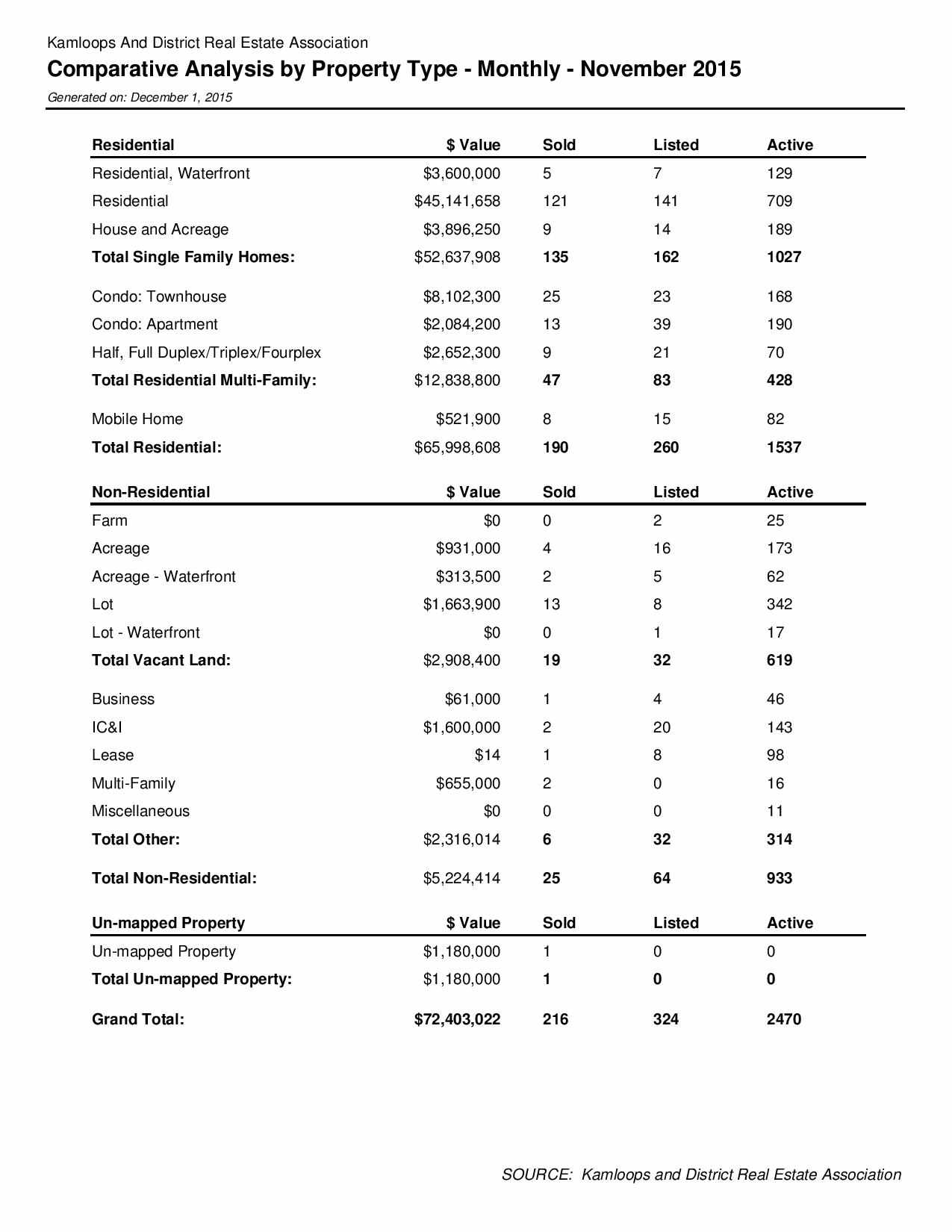

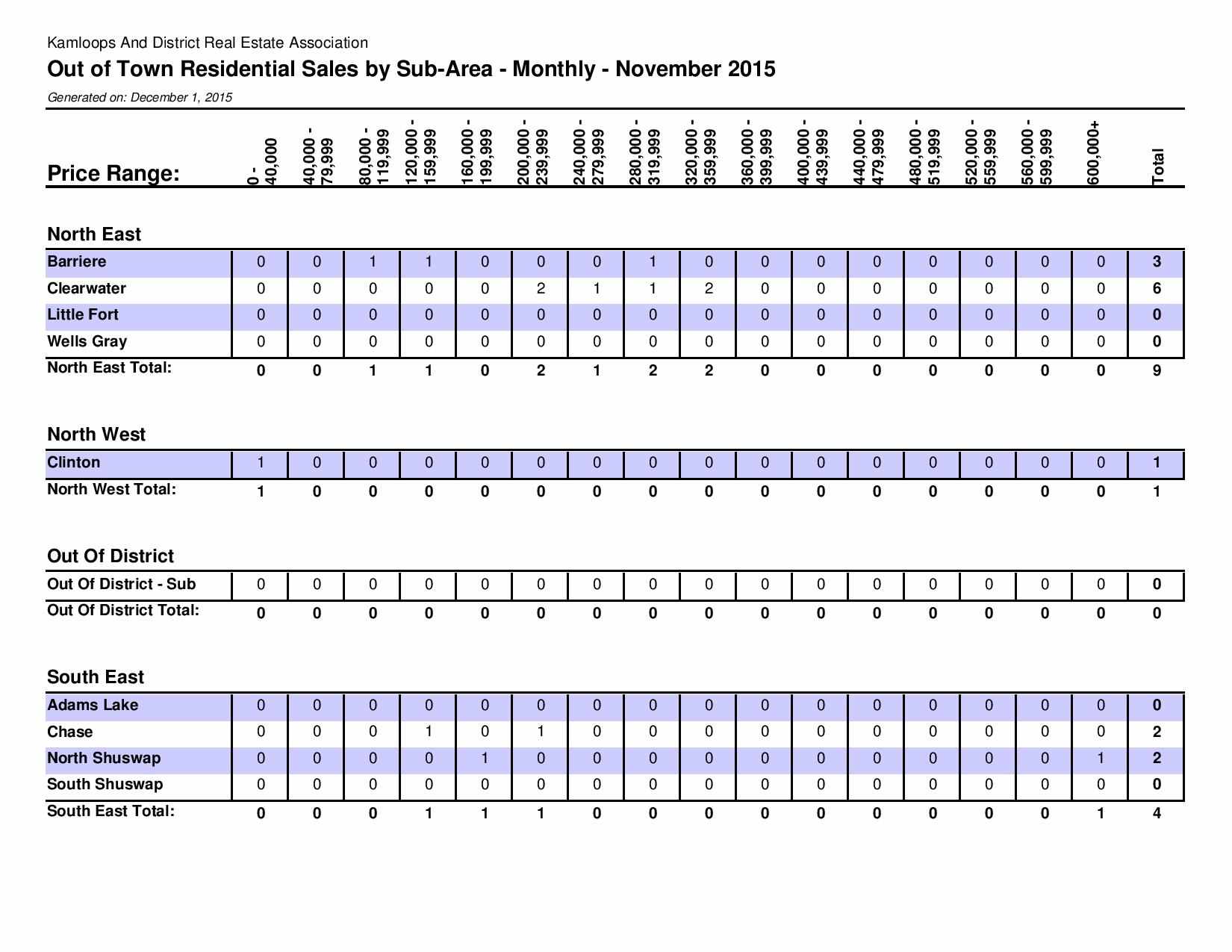

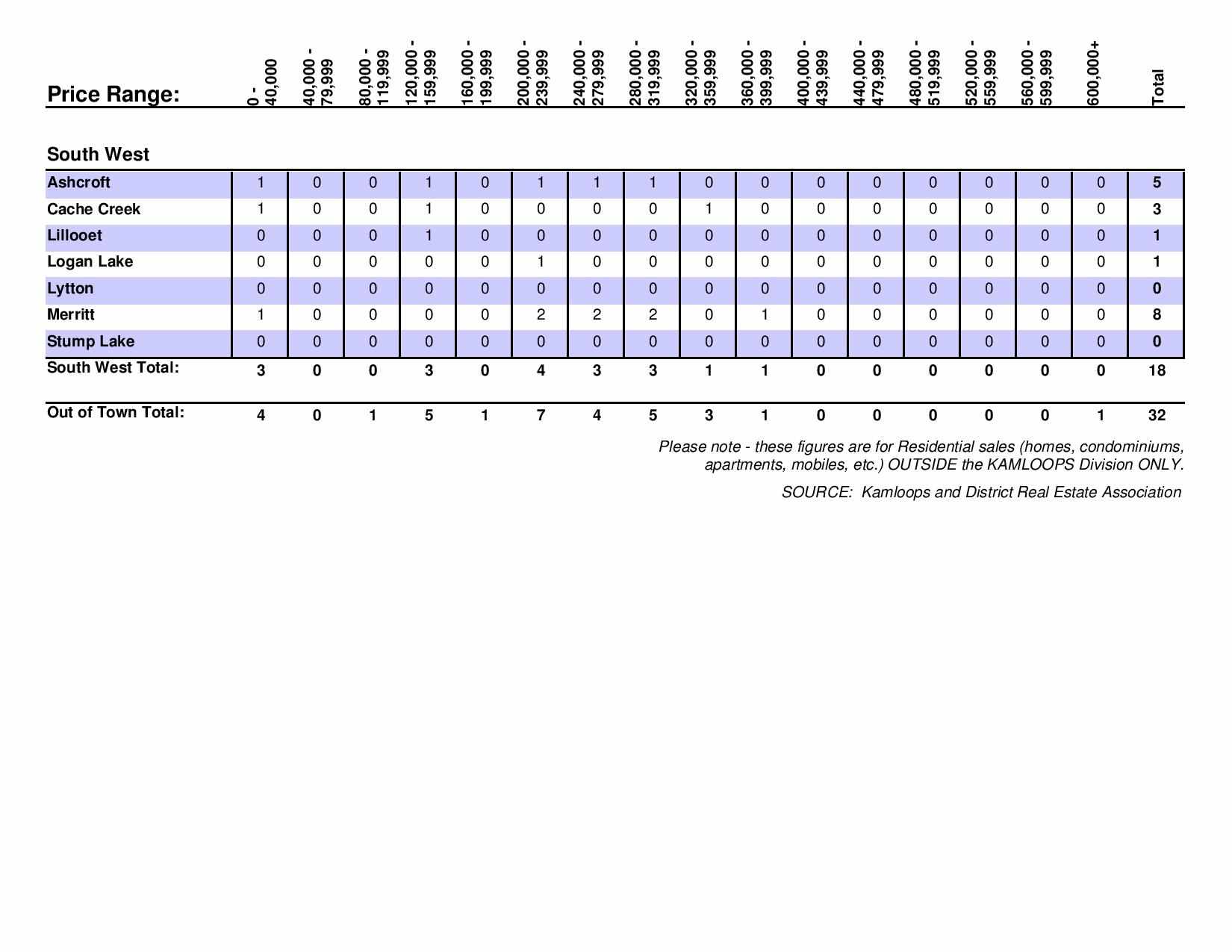

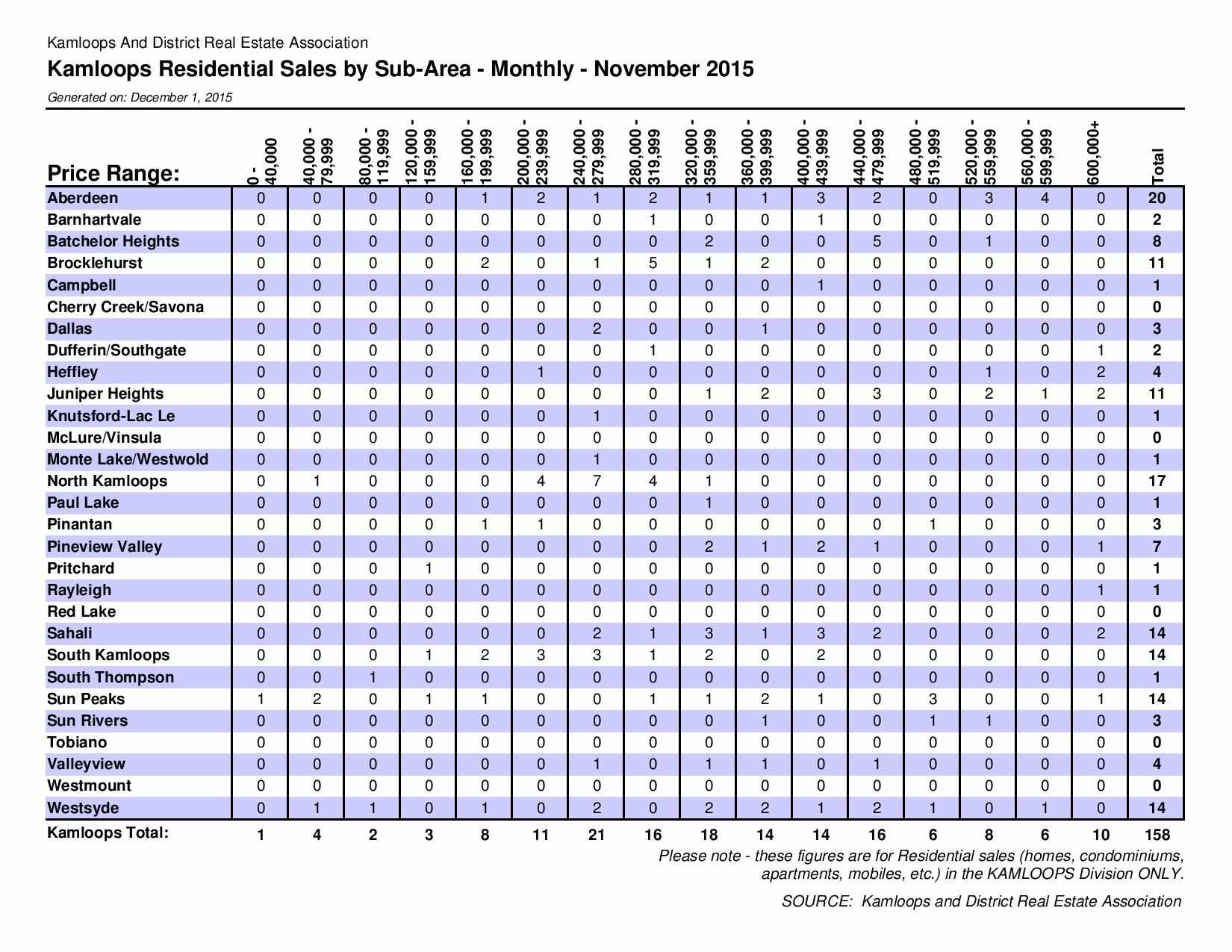

While real-estate sales cooled in December, the year 2015 marked an active real estate market in Kamloops.

Kamloops & District Real Estate Association recorded a 14 per cent increase in unit sales for the year, to reach almost 2,600 units. For December, typically one of the slowest months of the year, the market saw a nine per cent decrease in units sold.

Prices remain moderate, with the median price for a single-family home in Kamloops reaching $375,000. That monthly number can fluctuate widely due to the small monthly sample size. In November, the median price was $393,000.

For the year, the most active neighbourhood for sales was Brocklehurst, followed by Aberdeen and Sahali.

Neighbourhood: Aberdeen, Kamloops, B.C. Real Estate. Aberdeen is a desirable area of Kamloops to live. It is located on the south side of the valley bordered by Highways 5A (the Old Merrit highway) to the east and the Trans Canada Highway to the north. Pineview and Dufferin are to the west of Aberdeen, Southgate to the north west and Sahali (Upper and Lower) is located to the east and north east. Aberdeen stretches up the south slope fairly high giving it’s residents fantastic views of the city.

Properties & Real Estate

Aberdeen has a many choices for residential homes. Lower Aberdeen is mainly multi-unit condominiums and townhouses with the exception of a couple small enclaves of single family homes such as the Gloaming Drive area known as Gloaming Ridge. In the upper Aberdeen area there are larger single family dwellings and townhouses. The neighbourhoods north of Aberdeen Drive and east of Pacific are mature neighbourhoods with older homes. Many of the homes are executive type homes, with over 2,000+ square feet of living space and mainly flat use-able yards. There are a number of cul-de-sacs in this area making it a very desirable family area.

The area above Aberdeen drive is a newer development relative to the northern area of Aberdeen. The homes range in age from just a year old to a couple decades old. The lot sizes in this area vary due to some of the steep slopes that the homes sit on. They do tend to be on the smaller size with low maintenance yards.

A more mature neighbourhood with large executive homes often larger than 4,000 square feet can be found in Glenhmour Estates. This area is found off of Howe road on the west side of Pacific Way. Homes often are situated on large estate lots approximately a half acre in size.

There is a bare land strata mobile home park on Howe Road in Aberdeen called Aberdeen Glen Village. Homes range in size and age in this park. Owners of these homes own the land their home sits on and pay a small strata fee monthly for water, sewer, road maintenance/snow removal and garbage services. This strata is very nice with a park like feeling surrounded by trees and wildlife.

To view homes for sale in 1555 Howe Road click here.

Aberdeen is home to a number of condo and apartment developments. The majority of these types of units can be found along Hugh Allan Drive. There are a few other buidings throughout Aberdeen, such as Harrison Views and the Villas which are home to condos of varying size and price point.

Townhouse units are predominantly found off of Pacific way and Hugh Allan. The units on Pacific Way are rancher style homes that appeal to homeowners not wanting many stairs.

There are a number of newer strata and bare land strata developments in Aberdeen. Cobblestone Pointe on Hugh Allan Drive, Pacific Ridge Estates on Pacific Way, The Villas on Van Horne Drive, Brighton Place on Kinross Place, Stirling Heights on Linfield Drive, Carradale Court and Livingston Court both on Aberdeen Drive.

To view Aberdeen townhouse, strata and condo apartments for sale click here.

One of the single family housing development in Aberdeen where you will find homes built after 2005 is the Aberdeen Highlands Development. It is located east of Pacific way and this is the eastern development area. The area consists of the streets Talbot Drive, Bentall Drive, Willowbrae Drive and Court, Galbraith Drive, Telford Place and Drive and Raeburn Drive. Aberdeen Hills Skyline Park is located very close to this development, just below Telford Drive and Telford Place.

The second phase of the Aberdeen Highlands Development is the “West Highlands”. It is located west of Pacific way using some of the Aberdeen Hills Golf Links Course which was an 18 hole golf course. In this development there are many different types of homes, single family homes, townhouses, duplexes, condo style homes, bare land strata and estate lots. There is also a community fire hall and small scale commercial spaces. Development begun on Linfield Drive, Crosshill Drive and Dunbar Drive spreading to further streets in the region. There are also a number of strata developments in this area called Carradale Court, Livingston Court (both on Aberdeen Drive), Stirling Heights (off of Linfield Drive) and Brighton Place (on Kinross Place).The strata developments are a combination of townhomes with smaller footprints and attached walls to detached single family bare land strata units.

Many areas of Aberdeen area have fantastic views. It can get a little foggy at times in the winter and Aberdeen does get more snow than other low lying areas. This is a small compromise that residents are willing to make for the desirable neighbourhoods and beautiful views.

Aberdeen houses a number of retailers including the Aberdeen Mall where you will find numerous stores. There are also a number of big box stores in the Aberdeen area including Staples, Best Buy, Sport Check, Chapters, Hudson’s Bay, Canadian Tire and Costco to name a few. Aberdeen is also home to many of the city’s hotels, mainly located on Rogers Way between Hugh Allan Drive and Highway 5A.

Cascades Casino is located in this area as well and it houses three restaurants as well as gaming.

There are a few areas where professional offices are located. Mainly in the shopping district around Aberdeen Mall. There are not as many services in the Aberdeen area as the Sahali and Southgate areas.

Schools

Aberdeen has two elementary schools. Aberdeen Elementary (2191 Van Horne Dr) and Pacific Way Elementary (2330 Pacific Way). There are two high schools that often school Aberdeen students, but are not in Aberdeen, Sahali Secondary and South Kamloops Secondary. For further information on the schools visit the School District #73 website.

Thompson Rivers University is located in Southgate. TRU is a fully accredited University and offers a variety of programs and courses to students in many different areas of study. Aberdeen often is an area popular with students attending TRU. It is close enough to the University making it easily accessible.

Recreation

There are a number of parks and green spaces in Aberdeen. Both elementary schools have play grounds for children to enjoy. There are also numerous hiking trails as some areas of Aberdeen back on to green belts.

Kenna Cartwright park is within a five to 10 minute drive of Aberdeen. This beautiful park has panoramic valley views and many hiking and biking trails for the whole family.

Tournament Capital Centre is located in Southgate which is only a five to 10 minute drive from any Aberdeen neighbourhood. TCC has many different facilities all in one building such as gymnastics, swimming, indoor track, fitness facility, courts and much more. There are also a number of sports fields that surround the facility.

Transportation

Aberdeen is serviced by BC Transit buses on a frequent and regular schedule. Click here to view the BC Transit website. Highway #1 is easily accessible to Aberdeen.

Some areas of Aberdeen are located minutes from the Trans Canada Highway #1 and access to the Coquihalla. There are multiple access points and the longest distance from access is approximately five to seven minutes.

The Kamloops Airport is under 19 kilometers from Aberdeen and is a 20 to 25 minute drive.

Campbell Creek is 20 minutes east of the Kamloops city centre and is home to the Kamloops Wildlife Park on Dallas Drive. Campbell creek is a beautiful, quiet area set up against the southern hills of Kamloops.

Properties & Real Estate

Many streets in Campbell creek are named after animals often found in the neighbouring Wilderness park: Cougar Road, Coyote Drive, Grizzly Crescent and Badger Drive. This area is comprised of single family homes, which are for the most part newer homes. The lot sizes do vary in this area, most of the lots are flat and usable.

Some residents do have homes that back on to the Wildlife park or park land offering the owners privacy.

There are two strata developments in Campbell Creek. Kermode Landing at 8960 Dallas Drive consists of walk up town homes that are attached and feature single car garages. This development was built in 2024 and 2025. The second strata development in Campbell Creek is located at 8800 Dallas Drive and it is called the Burrows. These units consist of detached bare land strata homes and semi-attached duplex style homes. Each of these homes have yards, single or double garages and feature a number of different layouts. There is a central walking loop and grassy space for the residents to enjoy.

Shopping

Residents shop in the Valleyview area where Save-On Foods grocery store, Shoppers Drug Mart and other smaller retailers are located. The Flying J and the Co-Op Gas Station are located 5 minutes from Campbell Creek. The Flying J has a gas station, convenience store and restaurant. There also is a smaller retail space in Dallas called the Dallas Town Centre located less than a 10 minute drive from Campbell Creek. Dallas Town Centre has a small grocery store, BC Liquor Store, Subway, Gas Station and a couple other smaller retailers.

Major shopping is located 20 to 25 minutes west of Campbell Creek in the Sahali, Aberdeen and Southgate areas of Kamloops.

Click here to view the listings in the Campbell Creek area.

Thompson Rivers University is a 25 minute drive from Campbell Creek. There is public transportation servicing the Campbell Creek area.

Recreation

The BC Wildlife Park is located seconds from Campbell Creek. This park offers many different activities for the whole family.

There are also hiking trails, a public boat launch near Lafarge and many other outdoors activities to enjoy nearby. Boaters can access the Shuswap Lakes along the south Thompson River.

There currently are not any playgrounds in the immediate area.

There are two golf courses located fairly close to Campbell Creek. Rivershore Golf Links is approximately a 10 minute drive from Campbell Creek along the South Thompson River.

Pineridge Golf Course sits along the side of the Trans Canada Highway #1 in Dallas and is a five minute drive from Campbell Creek.

Transportation

There is a bus route that services this area. The bus stop is on Dallas Drive which is within minutes from each home in this area. Click here to view the BC Transit website.

Access to the Trans Canada Highway #1 is minutes from Campbell Creek making it easy to get around.

The Kamloops Airport is a 35 minute drive North West from Campbell Creek.

Click here for real estate listings in the Campbell Creek or Kamloops area.

To read more about other neighbourhoods click the link below:

Valleyview and Barnhartvale led city neighbourhoods in a 2015 assessment marked by continued moderate growth for Kamloops and the region.

Valleyview and Barnhartvale led city neighbourhoods in a 2015 assessment marked by continued moderate growth for Kamloops and the region. Neighbourhood: Aberdeen, Kamloops, B.C. Real Estate. Aberdeen is a desirable area of Kamloops to live. It is located on the south side of the valley bordered by Highways 5A (the Old Merrit highway) to the east and the Trans Canada Highway to the north. Pineview and Dufferin are to the west of Aberdeen, Southgate to the north west and Sahali (Upper and Lower) is located to the east and north east. Aberdeen stretches up the south slope fairly high giving it’s residents fantastic views of the city.

Neighbourhood: Aberdeen, Kamloops, B.C. Real Estate. Aberdeen is a desirable area of Kamloops to live. It is located on the south side of the valley bordered by Highways 5A (the Old Merrit highway) to the east and the Trans Canada Highway to the north. Pineview and Dufferin are to the west of Aberdeen, Southgate to the north west and Sahali (Upper and Lower) is located to the east and north east. Aberdeen stretches up the south slope fairly high giving it’s residents fantastic views of the city. The area above Aberdeen drive is a newer development relative to the northern area of Aberdeen. The homes range in age from just a year old to a couple decades old. The lot sizes in this area vary due to some of the steep slopes that the homes sit on. They do tend to be on the smaller size with low maintenance yards.

The area above Aberdeen drive is a newer development relative to the northern area of Aberdeen. The homes range in age from just a year old to a couple decades old. The lot sizes in this area vary due to some of the steep slopes that the homes sit on. They do tend to be on the smaller size with low maintenance yards. There is a bare land strata mobile home park on Howe Road in Aberdeen called Aberdeen Glen Village. Homes range in size and age in this park. Owners of these homes own the land their home sits on and pay a small strata fee monthly for water, sewer, road maintenance/snow removal and garbage services. This strata is very nice with a park like feeling surrounded by trees and wildlife.

There is a bare land strata mobile home park on Howe Road in Aberdeen called Aberdeen Glen Village. Homes range in size and age in this park. Owners of these homes own the land their home sits on and pay a small strata fee monthly for water, sewer, road maintenance/snow removal and garbage services. This strata is very nice with a park like feeling surrounded by trees and wildlife. The second phase of the Aberdeen Highlands Development is the “West Highlands”. It is located west of Pacific way using some of the Aberdeen Hills Golf Links Course which was an 18 hole golf course. In this development there are many different types of homes, single family homes, townhouses, duplexes, condo style homes, bare land strata and estate lots. There is also a community fire hall and small scale commercial spaces. Development begun on Linfield Drive, Crosshill Drive and Dunbar Drive spreading to further streets in the region. There are also a number of strata developments in this area called Carradale Court, Livingston Court (both on Aberdeen Drive), Stirling Heights (off of Linfield Drive) and Brighton Place (on Kinross Place).The strata developments are a combination of townhomes with smaller footprints and attached walls to detached single family bare land strata units.

The second phase of the Aberdeen Highlands Development is the “West Highlands”. It is located west of Pacific way using some of the Aberdeen Hills Golf Links Course which was an 18 hole golf course. In this development there are many different types of homes, single family homes, townhouses, duplexes, condo style homes, bare land strata and estate lots. There is also a community fire hall and small scale commercial spaces. Development begun on Linfield Drive, Crosshill Drive and Dunbar Drive spreading to further streets in the region. There are also a number of strata developments in this area called Carradale Court, Livingston Court (both on Aberdeen Drive), Stirling Heights (off of Linfield Drive) and Brighton Place (on Kinross Place).The strata developments are a combination of townhomes with smaller footprints and attached walls to detached single family bare land strata units. Many streets in Campbell creek are named after animals often found in the neighbouring Wilderness park: Cougar Road, Coyote Drive, Grizzly Crescent and Badger Drive. This area is comprised of single family homes, which are for the most part newer homes. The lot sizes do vary in this area, most of the lots are flat and usable.

Many streets in Campbell creek are named after animals often found in the neighbouring Wilderness park: Cougar Road, Coyote Drive, Grizzly Crescent and Badger Drive. This area is comprised of single family homes, which are for the most part newer homes. The lot sizes do vary in this area, most of the lots are flat and usable.

The BC Wildlife Park is located seconds from Campbell Creek. This park offers many different activities for the whole family.

The BC Wildlife Park is located seconds from Campbell Creek. This park offers many different activities for the whole family.