Author: Kirsten Mason

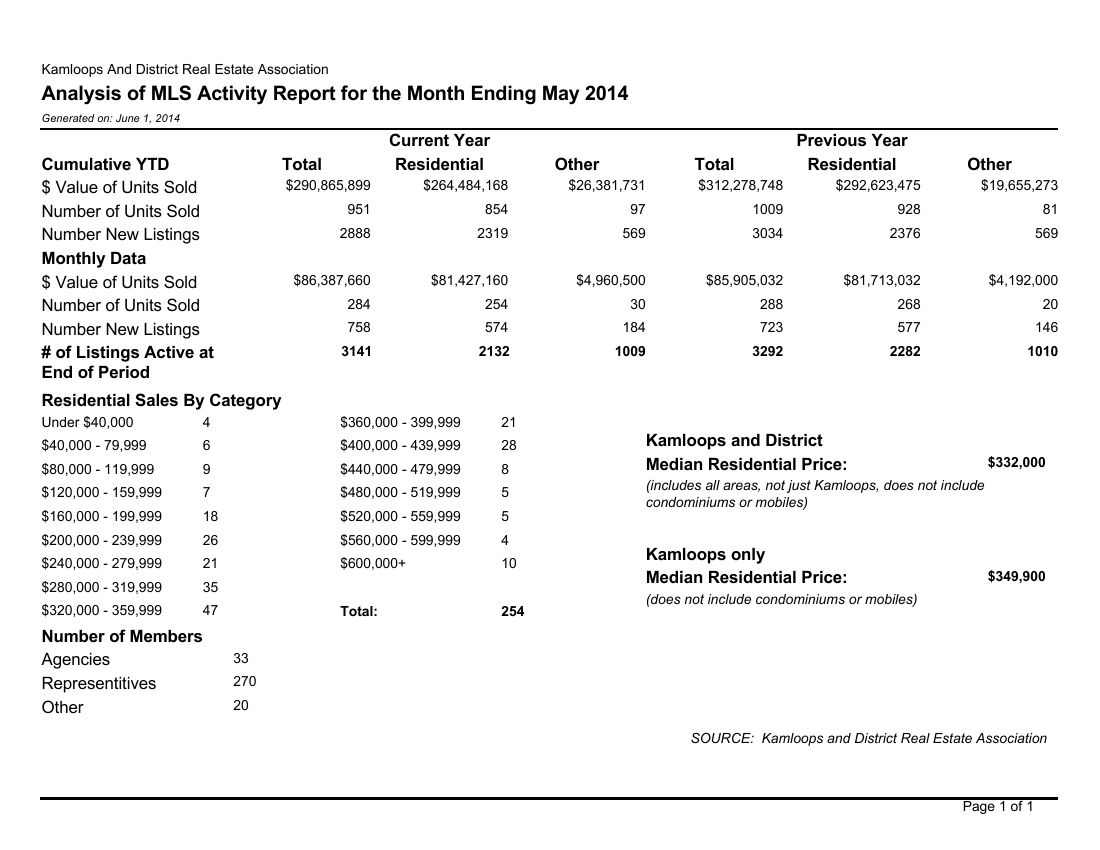

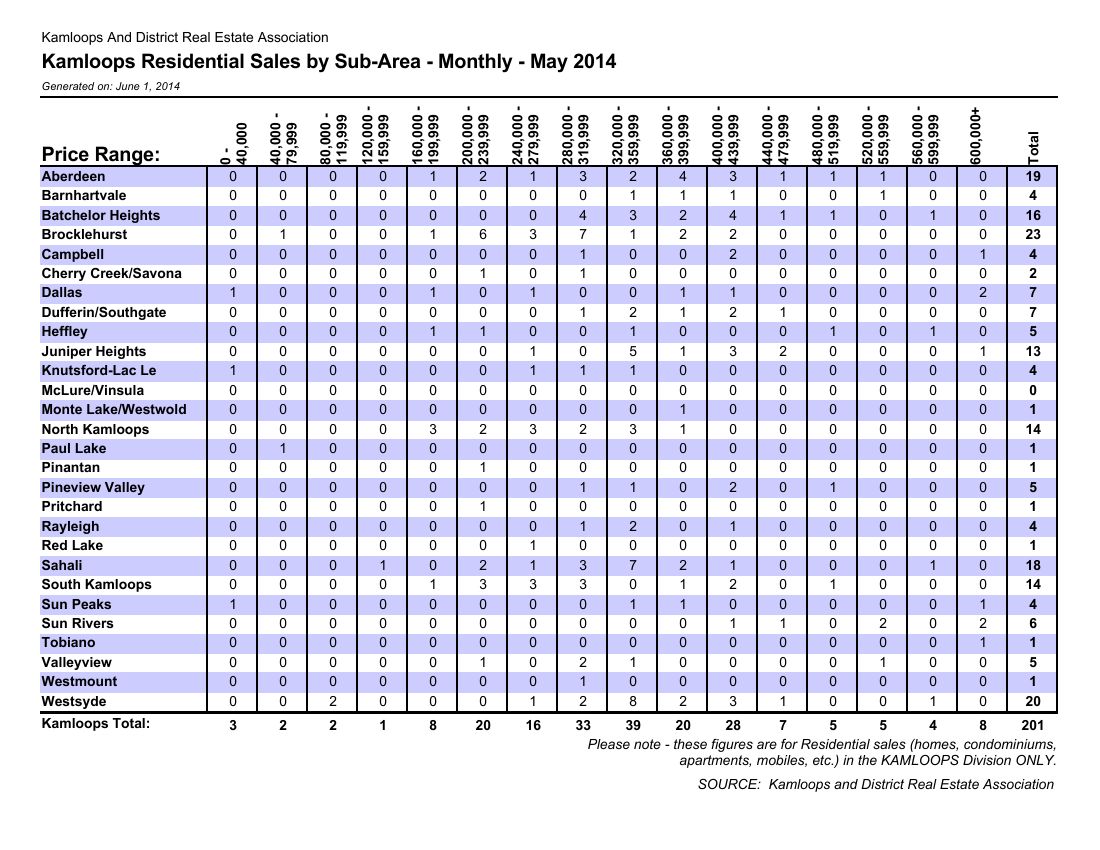

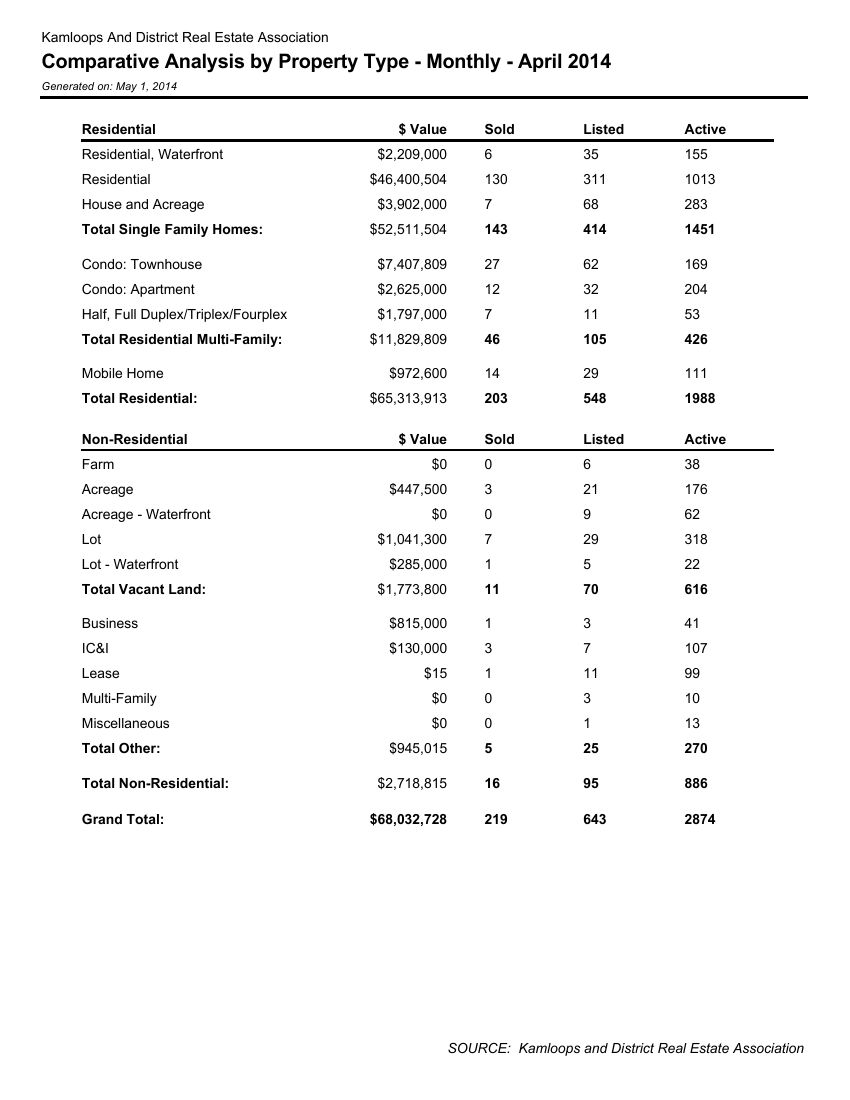

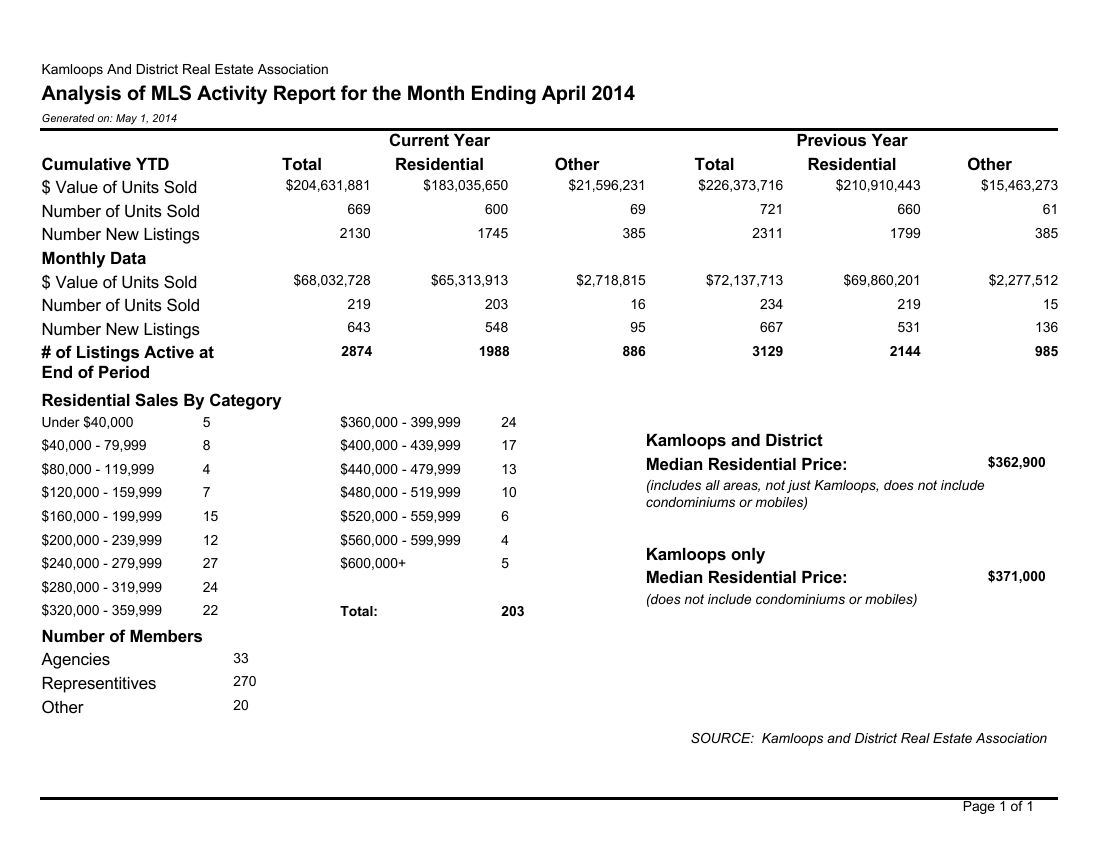

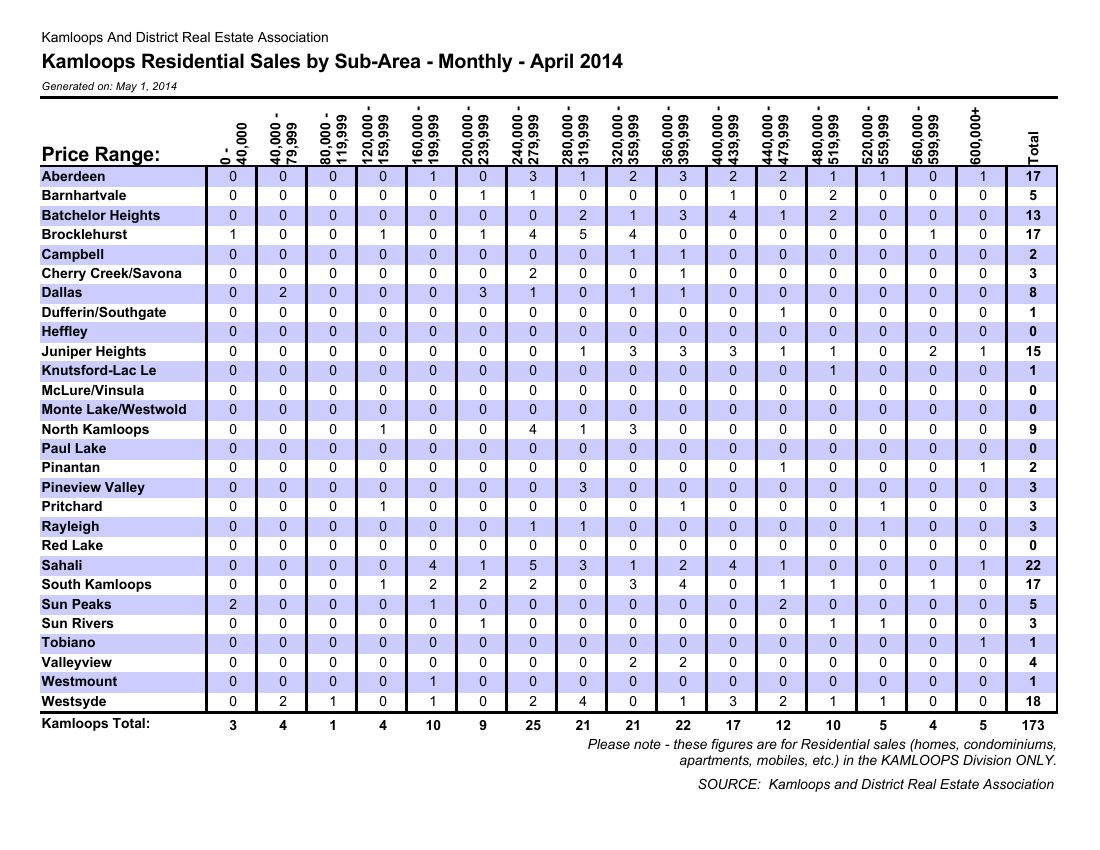

Kamloops District Real Estate Associations Statistics For April 2014

Housing Demand Forecast to Rise Through 2015, BCREA

Housing Demand Forecast to Rise Through 2015, BCREA. I have included the BC Real Estate Association’s report for this month. BCREA Chief Economist Cameron Muir discuss the April 2014 statistics. Muir points out historically low mortgage interest rates, population growth, employment growth and upturn in net migration are all contributing factors to the increased housing demand. See video below and full article from BCREA is included below the video.

Vancouver, BC – May 15, 2014. The British Columbia Real Estate Association (BCREA) released its 2014 Second Quarter Housing Forecast today.

BC Multiple Listing Service® (MLS®) residential sales are forecast to increase 5.2 per cent to 76,700 units this year, before increasing a further 6.7 per cent to 81,800 units in 2015. The five-year average is 75,400 unit sales, while the ten-year average is 84,800 unit sales. A record 106,300 MLS® residential sales were recorded in 2005.

“BC Home sales are expected to trend higher this year and in 2015, as stronger economic conditions both at home and abroad bolster consumer demand,” said Cameron Muir, BCREA Chief Economist. “While historically low mortgage interest rates are a key market driver, population growth led by a strong upturn in net migration and more robust employment growth are expected to generate additional housing demand.”

The average MLS® residential price for the province is forecast to increase 4.3 per cent to $560,500 this year and a further 2 per cent to $571,500 in 2015. Increasing consumer demand combined with fewer homes for sale has created balanced market conditions in most BC regional markets, resulting in home price appreciation more in line with overall consumer price inflation.

CMHC to Limit Mortgage Insurance Product Offerings Effective May 30; CMHC Will Stop Offering Mortgage Insurance on Second Homes

This article appeared on CBC.ca on April 26th, 2014. CMHC to limit mortgage insurance product offerings Effective May 30, CMHC will stop offering mortgage insurance on second homes

![]() Canada Mortgage and Housing Corporation will no longer offer mortgage insurance on second homes, the crown corporation said on Friday.

Canada Mortgage and Housing Corporation will no longer offer mortgage insurance on second homes, the crown corporation said on Friday.

It will also discontinue selling mortgage insurance to self-employed people without third-party income validation. The new limitations mean borrowers will also no longer be able to act as co-borrowers on other applications.

These changes, which will take effect on May 30, are part of the ongoing review of the mortgage loan insurance business. CMHC said self-employed Canadians can still qualify for insured financing with a validation of their income using traditional methods.

As well, the two products will still be available to those who submit requests prior to May 30, regardless of the closing date of the home purchase.

CMHC said these two products account for less than three per cent of its insured business volumes in units. “Given the limited use of these products, their discontinuation is not expected to have a material impact on the housing market,” CMHC said in its release.

The changes come as Canadian home buyers face an increase in mortgage insurance premiums.

In February, CMHC announced it would hike premiums for default insurance by an average of 15 per cent effective May 1. The increase would hit buyers who have a downpayment of less than 20 per cent.