BCREA Housing Market Update September 2018

BC Real Estate Association (BCREA) Chief Economist Cameron Muir discusses the August 2018 statistics.

MLS Listings, News & Statistics

BC Real Estate Association (BCREA) Chief Economist Cameron Muir discusses the August 2018 statistics.

Vancouver, BC – September 13, 2018. The British Columbia Real Estate Association (BCREA) reports that a total of 6,743 residential unit sales were recorded by the Multiple Listing Service® (MLS®) across the province in August, a 26.4 per cent decrease from the same month last year. The average MLS® residential price in BC was $669,776, down 1.2 per cent from August 2017. Total sales dollar volume was $4.5 billion, a 27.3 per cent decline from August 2017.

“The downturn in housing demand induced by the mortgage stress-test is now largely behind us,” said Cameron Muir, BCREA Chief Economist. “The BC housing market is evolving along the same path blazed by Ontario and Alberta, where the initial shock of the mortgage stress-test is already dissipating, leading to increasing home sales.”

Year-to-date, BC residential sales dollar volume was down 19.9 per cent to $41 billion, compared with the same period in 2017. Residential unit sales decreased 21.3 per cent to 57,674 units, while the average MLS® residential price was up 1.7 per cent to $719,064.

Here is a list of all the areas of Kamloops that have new residential housing developments. These developments consist of multi-family condominiums, townhouses, duplex units, bare land strata developments and single family homes. To view all home listings and properties for sale in Kamloops click here.

Here is a list of all the areas of Kamloops that have new residential housing developments. These developments consist of multi-family condominiums, townhouses, duplex units, bare land strata developments and single family homes. To view all home listings and properties for sale in Kamloops click here.

Brighton Place (1323 Kinross Drive) is Aberdeen’s newest single family (bare land strata) subdivision. This development features 2 and 3 bedroom plans. There will be 38 single family detached homes, duplex style and 4 plex style homes. Located off of Linfield Drive, a short walk to the Aberdeen Elementary School. This development is slated to be complete in 2020.

Carradale Court (1250 Aberdeen Drive) is one of the newer bare land strata developments in the Aberdeen highlands area. This development features 2 and 3 bedroom plans. There are 40 single family detached homes in this development. Located in the West Highland Development on Aberdeen Drive and is across from the Aberdeen Elementary School. This development is complete and resale units do come on the market periodically. Homes in this development were built between 2012 and 2014.

Cobblestone Pointe (770 Hugh Allan Dr) This development consists of 20 duplex style homes in a bare land strata. They back on to a green belt and will have valley and mountain views. It is located on Hugh Allan and Highway 5a (old Merritt Highway). These homes were built between 2011 and 2013. Resale units do come available on occasion, it s a popular development.

Harrison Views (1200 Howe Rd) is a new condo style development on the corner of Harrison Place and Howe Road in Aberdeen. Each unit comes with stainless steel appliances and granite countertops. There are one and two bedroom units with beautiful valley and river views. This condo building was built in around 2013.

Livingston Court (1325 Aberdeen Dr) is a newer multi-family townhouse development in the Aberdeen West Highland area. These homes consist of two bedroom and den as well as three bedroom units. Some of the units back on to green space and have nice valley and mountain views. These homes have nice open floor plans and lots of natural light. They were built between 2013 to 2016.

Pacific Ridge Estates (2160 Pacific Way) is a new development on Pacific way at Links Way. It is in the beginning stages of development and will feature 24 units. It is a gated community with beautiful valley views. It is located among many walking trails and close to shopping and schools. These homes are higher end rancher style homes with a mix of daylight walk out basements and below grade basements. This development features nice green spaces and most units are duplex style with one unit fully detached and one row of 3 units. These units completed construction in 2018.

The West Highland development is located at the intersection of Aberdeen Drive and Pacific Way. This development features a variety of dwellings including single family and multi-family homes. Phase one of the development includes 34 single-family lots, two multi-family sites and a mixed-use commercial-residential site.

To view all homes and properties for sale in Aberdeen click here.

Plateau at Riverbend is situated in the Saddleback Hills and is located north of Batchelor Drive off of Stagecoach Drive. This area is one of the newest single family developments in Batchelor and consists of brand new homes and serviced building lots. These homes and lots are found on Saddleback Drive, Latigo Drive and Doubletree Crescent.

Saddleback Hills is located north of Batchelor Drive. Stagecoach Drive and Saddleback Drive are two streets in Batchelor where this particular development will be found. There are a variety of homes for sale such as single family detached homes, bare land strata detached homes and duplex style bare land strata homes.

Quails Roost Court is located off of Quail Drive in Batchelor Heights. This is one of the newest developments in Batchelor. The homes are perched on top of a hill and boast beautiful views of the river and valley below.

The Views at Saddleback (900 Stagecoach Dr) is located at the foot of Saddleback Drive off of Grasslands Boulevard. This is a bare land 48 unit strata development and features single family detached homes and duplex style homes. Many of the units in this development feature valley and river views. Units in this development were built as early as 2008 and completed in 2013.

For more info about Batchelor Heights Click here.

To view all homes and properties for sale in Batchelor Heights click here.

Crestline Park (2592 Crestline St) This Bare Land Strata development is located off of Crestline Street in Brocklehurst. This strata has homes with open modern floor plans and feature three floor plans, rancher style, basement entry and two storey. All homes have their own small fenced yards. There are nice views of the hills and walking trails are close by. Each home has a single car garage and two parking stalls. Units were built between 2011 and 2013.

Mayfair & Riverbend are seniors oriented independent living condos with lots of amenities. There are also support services offered at this development. Amenities include fitness centre, theatre room, games room, workshop, community garden & more. The complex is pet friendly and wheelchair accessible. It is very close to shopping and transportation.

Suncrest Place (1923 Parkcrest Ave) This smaller style bare land strata development features duplex style homes that have nice modern finishes, single car garages and nice yards. There will only be 10 units in this development. Development on this site began in 2013 and continues through 2018.

Sunset Ridge (1900 Ord Rd) is a development off of Ord Road set against the northern hills in Brock. This is a leasehold development with low bare land strata fees. There is the option to pay out the lease to transfer the property to a freehold interest. These homes are built green with low-e windows, 30 year roof and high efficiency furnace. All the homes in this development are modular/manufactured homes that sit on a foundation. Some homes do have a basement.

West Briar Estates development is located west of Crestline Street in Brock. This area is mainly single family detached homes on lots that are a minimum of 5,000 square feet. The homes built in this area are predominantly basement entry style homes with two car garages and open floor plans. There are a few ranchers also built in this area. There are not any more lots available and some homes are now coming up as re-sale homes in this area.

For more info about Brock click here.

Campbell Creek Village is located close to the Wildlife Park 20 minutes from the Downtown core. There are a number of building lots on Dallas Drive, Badger Drive and Badger Place available for purchase including cul-de-sac lots. New homes are also available for purchase. Hiking trails surround this beautiful area of Kamloops.

The Burrows (8800 Dallas Drive) is Campbell Creek’s newest bare land strata development featuring duplex and single family style homes. This community began construction in 2016 and continues at this time. The Burrows is located 15 minutes from downtown Kamloops and a short drive from shopping, schools and amenities.

Dallas Town Centre is a new development located on Dallas Drive. This development is a mix of commercial and residential. Condominium units range in size from one bedroom, one bathroom to larger three bedroom, two bathroom units. These units are complete and ready for occupants.

For more information about Dallas click here.

Hidden Trails at Mount Dufferin is the newest subdivision in the Dufferin area. It is located at the end of Pacific way and is bordered by Kenna Cartwright park. There are numerous single family homes, lots (4 phases) and two multi-family developments. Rockress Drive is Phase 2 of this development and services are in for the new homes that will soon sit on these lots. There are a number of homes already built on Rocress Drive and more are being built monthly.

Orabella (1395 Prairie Rose Drive) is a luxury townhouse development in the Hidden Trails area of Dufferin. These are not entry level townhouses in terms of price, they are higher end homes and range in size. These units are surrounded by parkland, feature modern design and functional floor plans. Construction began on these units in 2015/2016.

For more info about Dufferin click here.

To view all homes and properties for sale in Brock, Campbell Creek, Dallas, Dufferin & Southgate click here.

Canyon Gate (1951 Qu’appelle Blvd) is one of the newest multi-family townhouse development in Juniper with construction beginning in late 2017. This development features homes that range in size from 2 to 3 bedrooms, single car garages and low maintenance living.

Coldwater Terrace (1939 Coldwater Dr) is a private bare land strata development nestled against the hillside in Juniper Heights. It is located in the West end of Juniper Heights and features single detached homes and duplex style homes. There are both rancher style homes and basement entry. Each home has a two car garage, 9 foot ceilings on both the main and basement levels and is fully landscaped.

The Juniper Benchlands area is located at the eastern portion of Juniper Heights. Many homes have breathtaking views that stretch as far as Kamloops Lake. There are a number of new homes built in this area as well as lots ready for development. This area is predominantly a single family detached development with larger, executive homes typically over 3,500 square feet in size. The newest streets in this area are Similkameen Place, Birkenhead Drive and Place, Cheakamus Drive and Place and Kicking Horse Drive.

Juniper West is located to the west of Highland Drive. Juniper West sits on the western portion of Juniper Heights and boasts beautiful views of the valley below. The newest stretch of Juniper West is along Coldwater Drive that was recently extended westward towards Rose Hill. There are also building lots on Galore Crescent. Many new, pre-existing homes that have been built over the past couple years are located on Stikine Street and Kechika Drive and Kechika Court. New, two storey duplexes are located on Highland Court. These homes are situated near the new commercial area of Juniper.

Silverwood Pointe (1993 Qu’appelle Blvd) is a townhouse development in the Juniper West area with basement entry, two storey and rancher style units. This development begun construction in 2015 and completed in 2018. Silverwood is located walking distance to the Juniper Ridge store, transportation, Kamloops Bike Ranch, park space and hiking trails. Juniper Ridge Elementary school is a short drive or 15 to 20 minute walk.

For more info about Juniper Ridge click here.

Golden Vista Suites (375 Cherry Ave) is a Seniors orientated development in North Kamloops. There are 46 freehold strata units in this development. There is a choice of studio and one bedroom apartment style living and there is also a common room and patio for socializing. There is a bonus of 55% reduction in property taxes for 10 years from the City of Kamloops. These units were built in 2010.

Library Square (689 Tranquille Rd) is a three phase strata condominium residences above the new North Kamloops Library and commercial complex. This new development is conveniently located between the North Hills Shopping Centre, the new Holiday Inn and Cottonwoods community centre. Each unit has a spacious maple kitchen, in-suite laundry, storage locker, a large balcony and underground secure parking. Currently Library Square is selling phase three. This complex is in a great location close to numerous amenities.

For more info about North Kamloops click here.

Copperhead Corner (1711 Copperhead Dr) is Pineview’s newest townhouse development. These homes are located on the corner of Copperhead Drive and Hugh Allan Drive. These homes are a two storey design with the garage under the main floor. Each unit comes with a single car garage, two bedrooms and two and a half bathrooms. Located within steps of walking trails, the park and transportation. All units have been sold in this development but will come up for resale.

The Landing (1850 Hugh Allan Drive) is a bare land strata development located on the corner of Hugh Allan Drive and Copperhead Drive in Pineview. This development began development in 2014 and completed sales in 2017.

For more info about Pineview click here.

Creston House: The Reach (885 University Drive) is the newest multi-family development in the Thompson Rivers University area. The Reach is a master planned community that will reconstruct 90 acres of TRU endowment lands into space that will house 7,500 residents over the next 20 years.

Landmark One, Landmark Two & Landmark Place (McGill Rd) is conveniently located across the street from the Thompsons Rivers University on McGill Street near Summit Drive in Southgate. The first phase is complete and features a four storey, 32,800 square foot building development. This development also includes about 9,000 square feet of retail space. Landmark Two is an extension of the first development and features 38 one and two bedroom units. The units range in size from 935 square feet to 1,400 square feet. Landmark Place is the highest of the condo towers and was completed in 2017/2018.

Mesa Estates at Sedona Pines development is on Azure Place, located in Upper Sahali. Homes here have stunning northern views of the mountains and valley below. This is a bare land strata development and consists of single family homes that are over 2,500 square feet.

Monarch Drive development is located between Springhill Drive and McKinnley Court. This new development consists of primarily single family homes. There are lots ready for development and new homes at various stages of completion.

Summit Pointe (1405 Springhill Drive) is a new condominium development on the corner of Springhill Drive and Summit Drive. The units in this development feature geothermal heating and cooling, excel custom kitchens, granite counter tops, six appliances and a common fitness facility. The units have beautiful northern views. There is also secure, underground parking. These units were built in 2009.

For more info about Sahali click here.

To view all homes and properties for sale in Juniper Ridge, North Kamloops, Pineview and Sahali click here.

Guerin Creek is a new high end development in South Kamloops just off of Summit Drive. Many of the homes have high end finishing and appliances. Current homes in Guerin Creek are two level designs with a basement. The lot sizes do vary. Many of these homes have amazing views of the Thompson River Valley looking north.

Hudsons Ridge is a single family development north of Thompson Rivers University and west of Summit Drive. Hudson’s Ridge features larger single family homes with gorgeous river and valley views. Edgehill Place is the first street that was developed in Hudson’s Ridge.

The Mosaic is located in the heart of South Kamloops. These units are built with high end materials such as hard wood floors, heated tile and custom kitchens. Features on demand hot water and stainless steel appliances. There is also secure underground parking and private entrances.

Arbutus Estates Villas have unobstructed views of the South Thompson River. Each unit features high end finishing such as hardwood flooring, granite counters and ceramic tile. There is a double garage and a security system. Each unit has over 1,200 square feet on the main floor with the same square footage in the basement.

The Mission Hill (975 Victoria St W) development is located on the south side of the Thompson river overlooking Victoria Street West and is west of the Overlander bridge. There is a choice of one, two and two bedroom plus den units with a gourmet kitchen and a large balcony perfect for entertaining. The development will feature walking paths, gathering spaces and lighting features. This development is located within walking distance of the Thompsons Rivers University and very close to the Kamloops downtown core.

The Royal Residence (315 St Paul Street) is one of the newest condo developments in Downtown Kamloops. These 1 and 2 bed homes each come with a Den, Deck and Parking stall. These units have easy access to all downtown amenities including restaurants, shopping, professional offices, banking, the Farmer’s Market, Sandman centre & Riverside park.

Sanoa Villas (370 9th Avenue) is located steps from Sagebrush Theatre, all levels of schooling for the kids and in a great neighbourhood. This multi-family townhouse development is in a very highly sought after area of Kamloops. There is a choice of 2 or 3 bedroom units and each home has a single car garage. These homes are located walking distance to many downtown amenities, farmers market and transportation.

For more info about South Kamloops click here.

Sienna Ridge (641 Shuswap Road E) is located 1 minute east of Sun Rivers on the shores of the South Thompson River and five minutes from Downtown Kamloops. This community features rancher style homes with two bedrooms on the main level including the master bedroom with full ensuite and walk in closet. There is an open great room floor plan with high ceilings and lots of windows for natural light. There are many gorgeous upgrades in each home with quartz counter tops throughout the main floor not only in the kitchen but also the bathrooms. Each property features all appliances and window coverings. Other features include main floor laundry with a dedicated laundry room, not a laundry closet! There is a two car garage and a full sized driveway to park those oversized pick up trucks. this development also has on site RV parking! Perfect for the lock and go lifestyle. All yard maintenance and landscaping included with the HOA fees. Click here to learn more.

Belmonte (512 Belmonte Dr) is a new Townhouse development located above the 10th fairway in Sun Rivers. These garden style townhomes are executive style with a ‘taste of Tuscany’. These homes are south facing and come in a variety of floor plans.

Golf Ridge Townhomes are low maintenance living where owners can lock up and go. These executive homes are are complete and ready for new owners. They feature granite countertops, stainless steel appliances, hardwood floors and crown mouldings.

Ironwood which is now selling (Phase I was sold out and they are currently selling Phase II), is bordered by natural areas on the west side of the development and Stoneridge Adult community on the east. Many of the homes sit on 6,500 to 12,000 square foot lots and are built in an “Old World” architectural style like an English country neighbourhood.

The Pointe, which is now selling lots, consists of unobstructed view lots with contemporary modern architecture. This is an adult orientated development. Located close to the Talasa development, the Pointe is in a great location with easy access.

Rio Vista (Rio Vista Place) is Sun River’s newest multi-family adult oriented development featuring single family detached homes. Each home comes fully landscaped and a number of homes feature gorgeous views of the river and valley. This development is for those looking for a lock and go lifestyle! Sit back and enjoy.

Talasa: There are three stages of the Talasa residential condominiums. Each building consists of four storeys. The units have stainless steel appliances, granite counter tops, walnut and charcoal themed flooring and luxurious contemporary accents throughout. Talasa units have geothermic heating and cooling systems and use sustainable materials and eco-sensitive initiatives. The Talasa development includes a shopping and restaurant development, exercise facilities and a residents club (phase 4). Phase 3 is complete.

Visao lots are located at the east end of Sun Rivers. They feature large executive lots with beautiful views of the valley and golf course. There are homes for sale currently in Visao in various stages of construction.

For more info about Sun Rivers click here.

To view all homes and properties for sale in South Kamloops, South Thompson Valley and Sun Rivers click here.

Courtland Park is located in the Orchards walk development on Valleyview Drive. These units are built green. The units have 3 bedrooms, 2.5 bathrooms, 9 foot ceilings and two car tandem garages. There are no age restrictions, pets and rentals are allowed in this development.

Orchards Walk is a bare land strata development located on Valleyview Drive. Orchards Walk consists of a number of single family homes that have small private yards. Homes range in size from two bedroom, two bathroom homes to much larger.

For more info about Valleyview click here.

Beachmount Estates located on Bank Road is a new single family development bordering the North Thompson River. Currently the site of “The Mansion” Beachmount Estates offers 34 building lots in phase 1 that are available for purchase. There are also a number of homes that are in the finishing stages and will be ready for occupancy in the next few months. Many homes have beautiful views of the river and easy access to the park and walking trails. This new development is located in the heart of Westsyde and is close to schools, transit and shopping.

Copperwood Estates (3031 Westsyde Rd) is a new development located on Westsyde Road. This bare land strata development consists of rancher style duplex homes and two storey duplexes. The ranchers have unfinished basements and over 1,000 square feet on the main floor and the two storey designs have over 1,500 square feet on two floors and no basement. Each home will have a single car garage. This development is sold out so Buyers will only have resale units to consider.

The Estates at Riverbend is a single family home development that sits above Westsyde Road minutes south of Westmount. Grasslands Boulevard is the main road that meets Westsyde Road. There are plans to eventually hook up Grasslands Boulevard in Batchelor Heights with Riverbend. The properties in this development have nice river views and are set against the Lac Du Bois Grasslands Park.

Rockliffe at Ida Lane is a bare land strata development near the Dunes golf course in Westsyde. This development mainly consists of larger single family homes. The homes have nice south east views of the city and hills.

Stansfield Road, Hayward Place and Bank Road are the site of the newest Westsyde development. There are a number of serviced building lots ready for new homes. The lots range in size from just over 4,000 square feet to over 7,000 square feet in size. They are located close to transportation, schools, parks and shopping.

Westlinks at the Dunes is a bare land strata development with fully detached homes that sit along the 5th fairway of the Dunes golf course. There is a combination of rancher style homes and two storey layouts. Homes range in size. There are also lots ready for development.

For more info about Westsyde click here.

To view all homes and properties for sale in Valleyview and Westsyde click here.

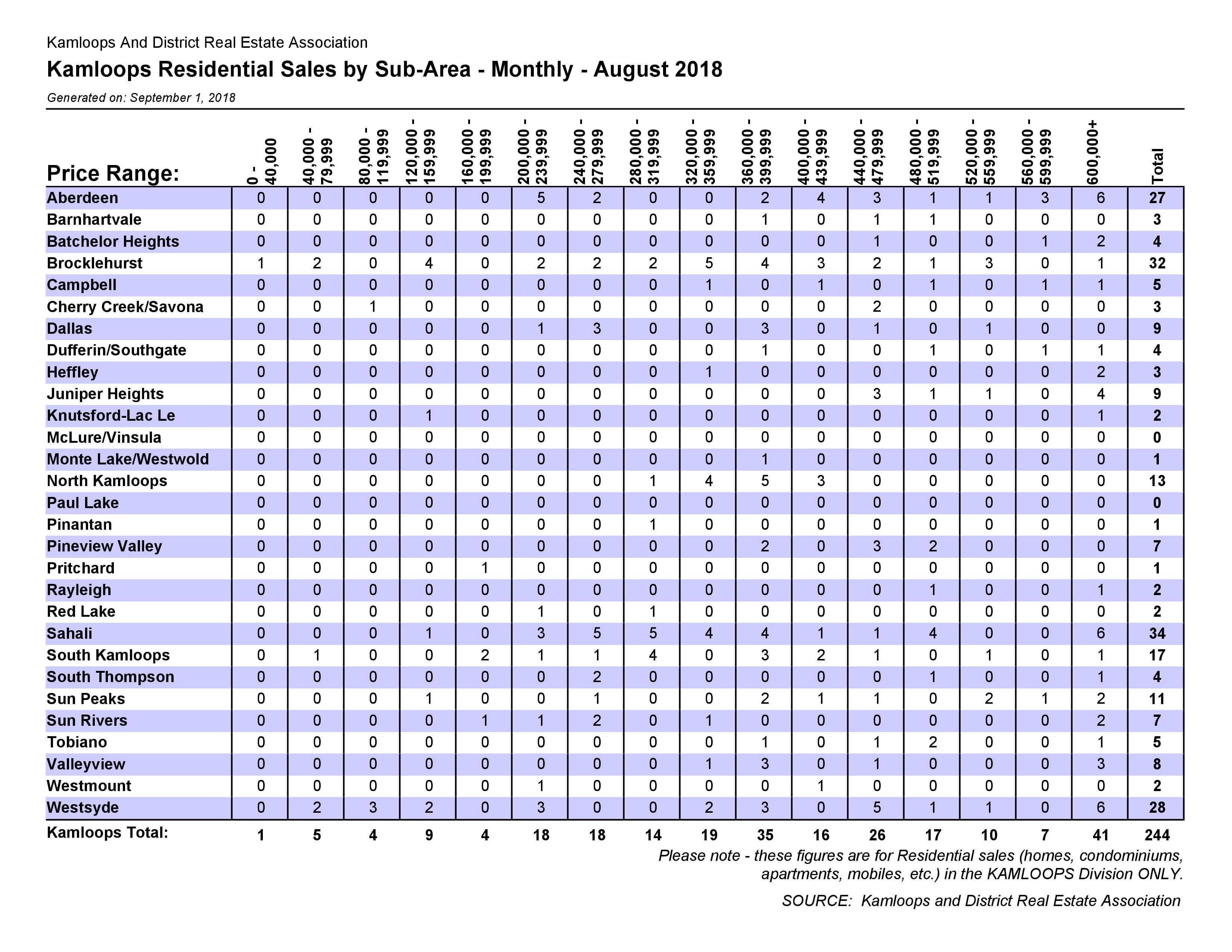

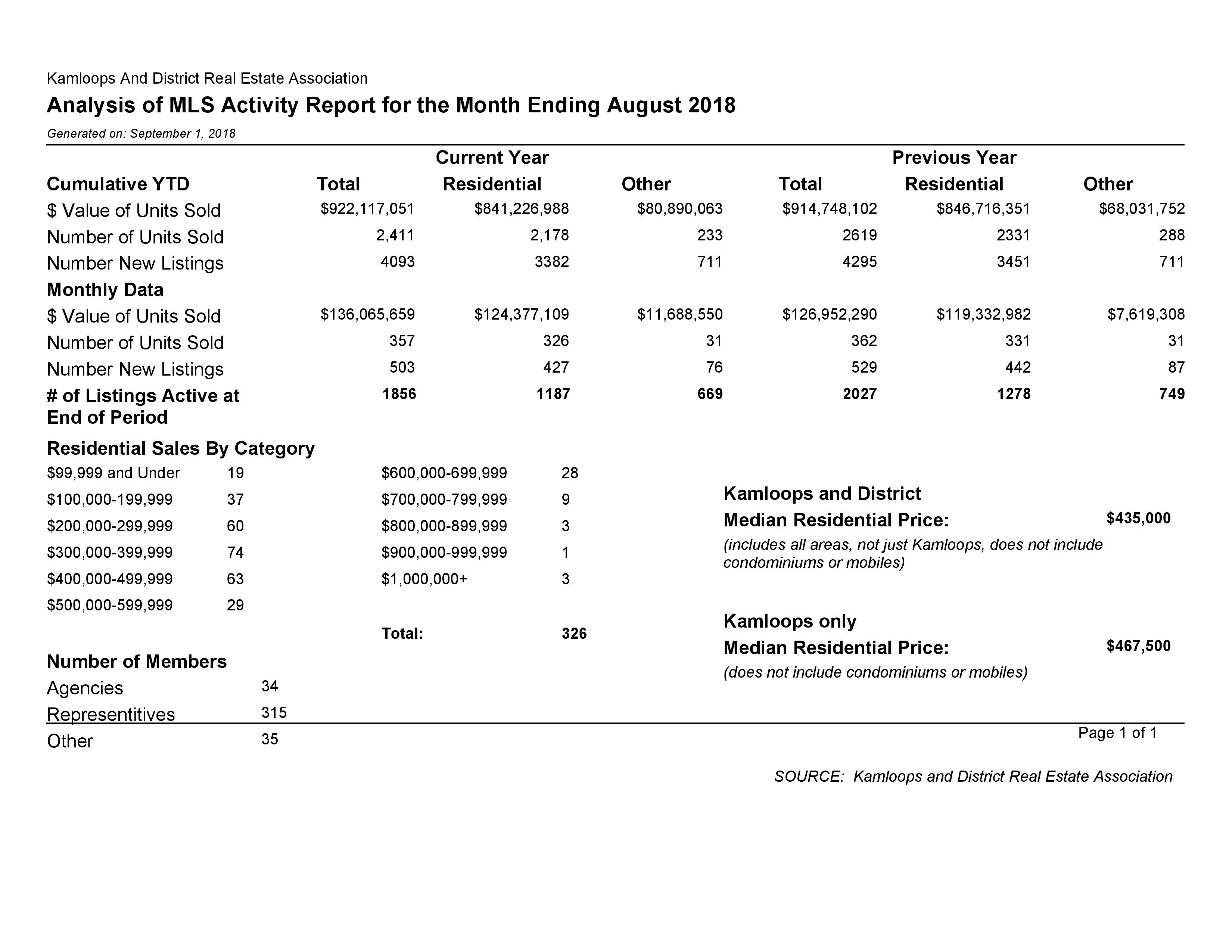

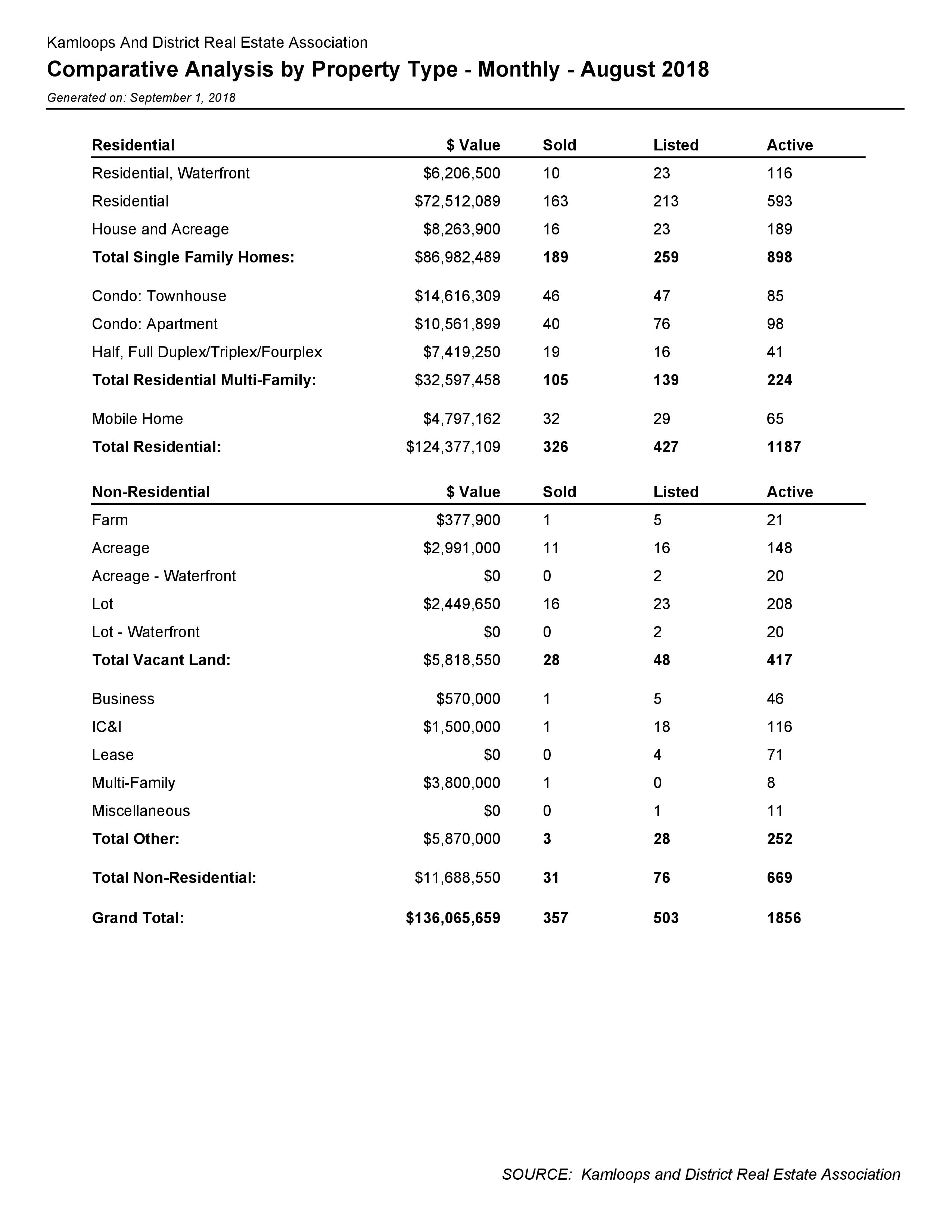

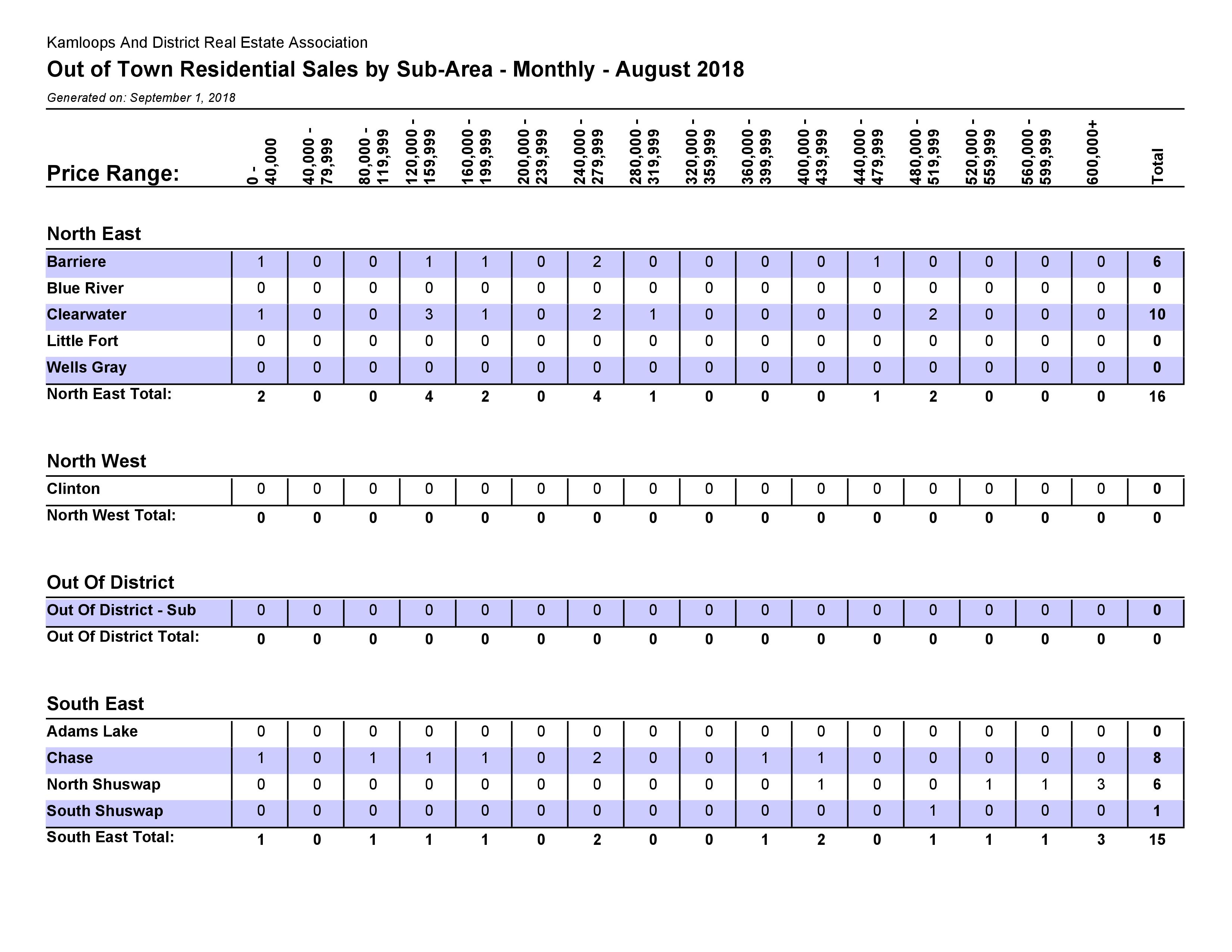

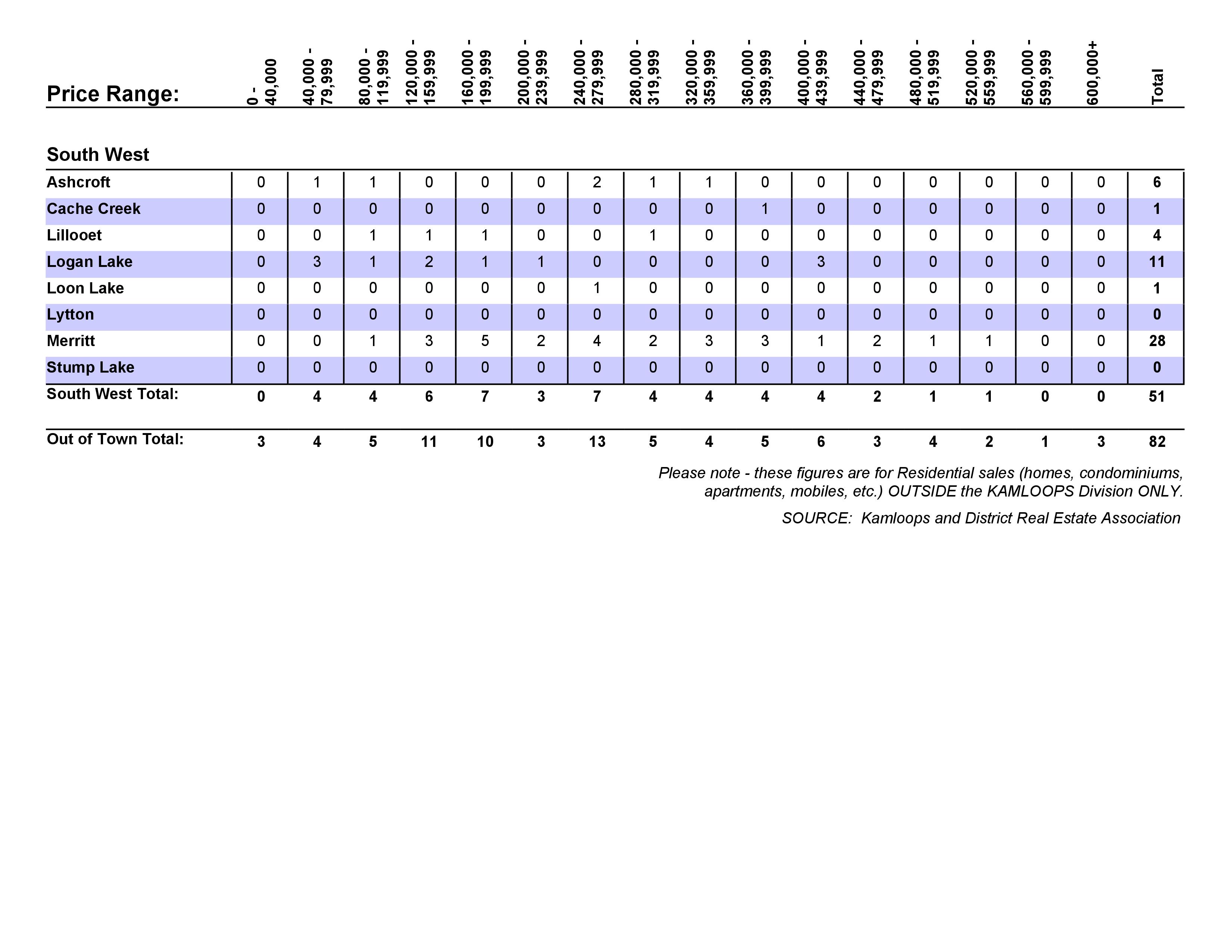

The Kamloops District Real Estate Association has released the latest Statistics for August 2018. Click on the image below to enlarge or PDF documents included in the links below.

PDF: Comparative Analysis by Property Type

PDF: Out of town Sales by Subarea