Housing Starts Steady as Market Prices Remain Competitive, Kamloops Daily News

This article appeared in the Kamloops Daily News on August 15th, 2013.

Kamloops is like the tortoise in the fabled race against the hare.

Kamloops is like the tortoise in the fabled race against the hare.

Slow but steady, the city has been growing with a relatively stable economy and moderate increases in population, unlike some communities that have experienced the rushing boom and then sluggish bust of others.

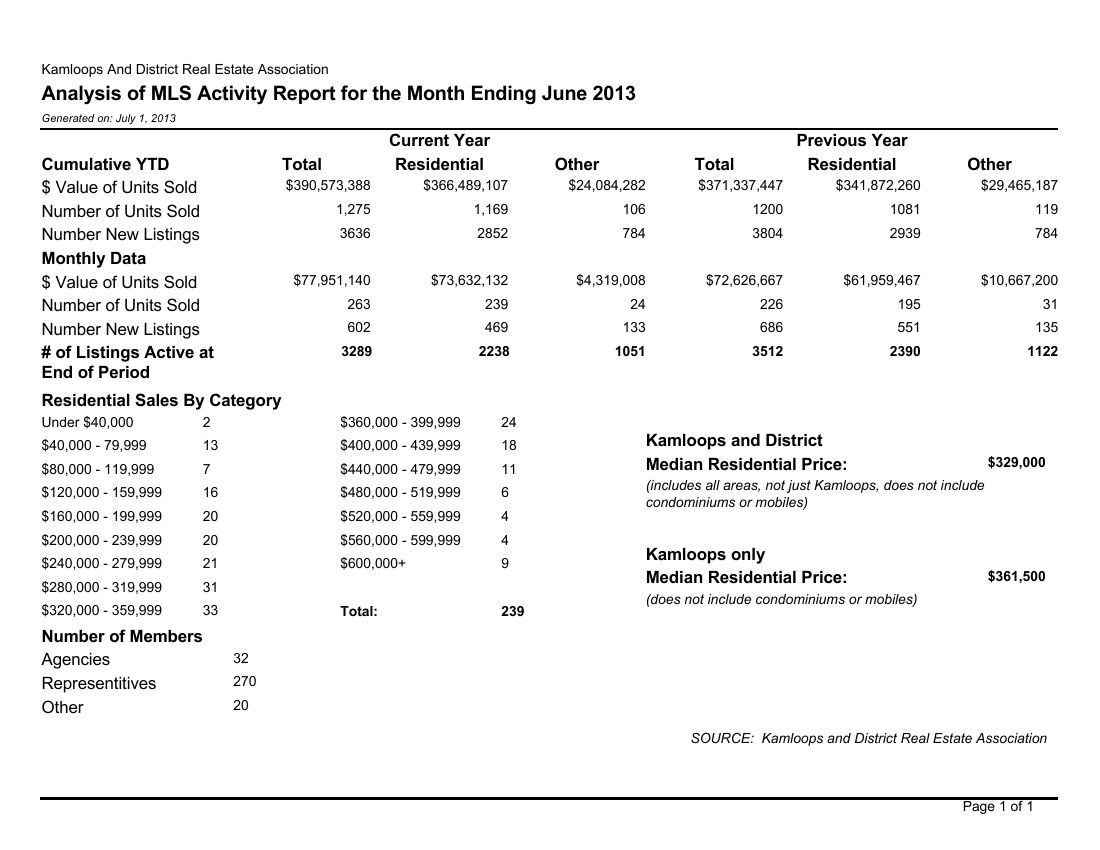

Canada Mortgage and Housing Corp. market analyst Paul Fabri said Thursday housing starts for the first half of 2013 in Kamloops have been close to those of the previous year.

In 2012, 317 homes were started between January and the end of July, while this year, that number is at 330.

“Kamloops overall has fared better in terms of new construction than some communities with resort housing or second homes,” such as parts of the Okanagan, he said.

Kamloops has also had stronger employment growth than some other centres, Fabri added.

He suggested single-family home construction hasn’t been as strong as multi-family because the market is competitive these days. He described the Kamloops economy as relatively stable, which has kept housing construction on an even keel.

“Overall, housing starts will reach my forecast for this year, which was 500 housing starts. That’s just slightly more than last year,” he said.

For 2014, Fabri predicts housing starts in Kamloops will reach 525 units.

On the other hand, Kelowna’s housing starts have dipped in the last few years, after taking a big drop during the 2008/2009 recession years. That’s because of a reduced demand for resort housing during that period, Fabri said.

“Kelowna hasn’t seen as robust employment growth as Kamloops has. That factor has helped maintain stable housing activity,” he said.

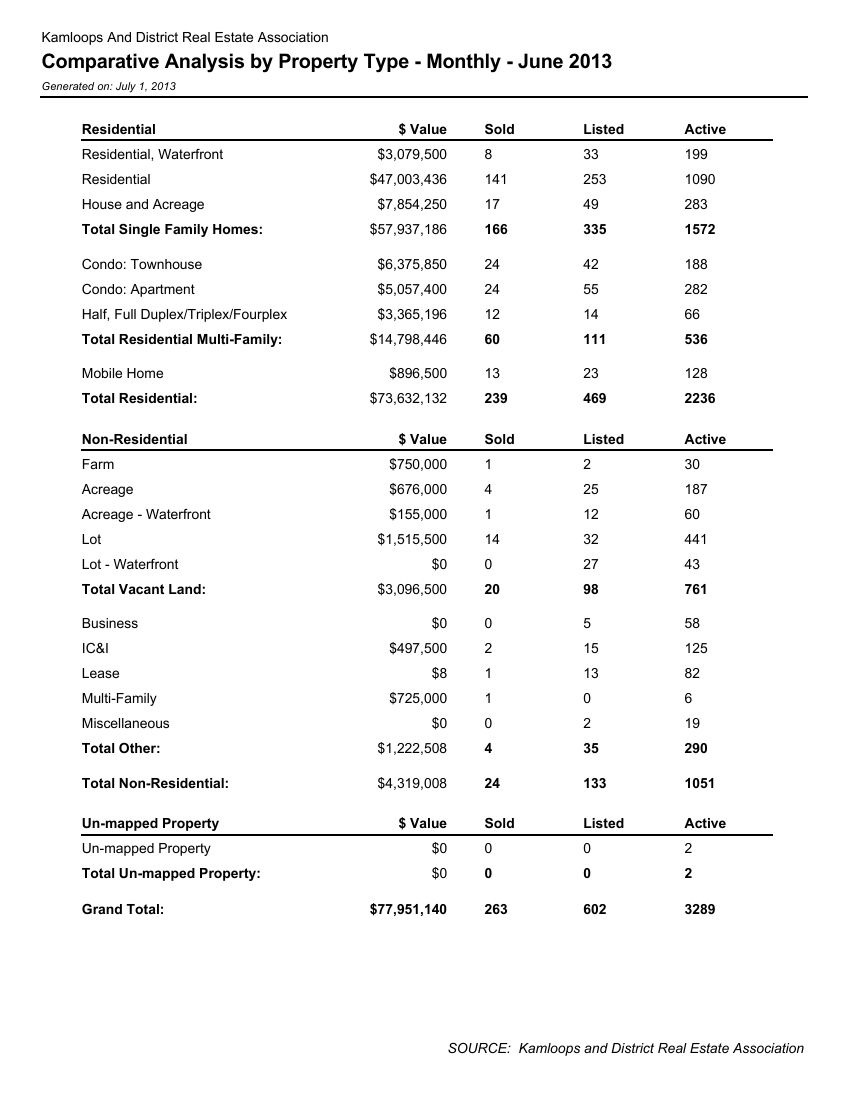

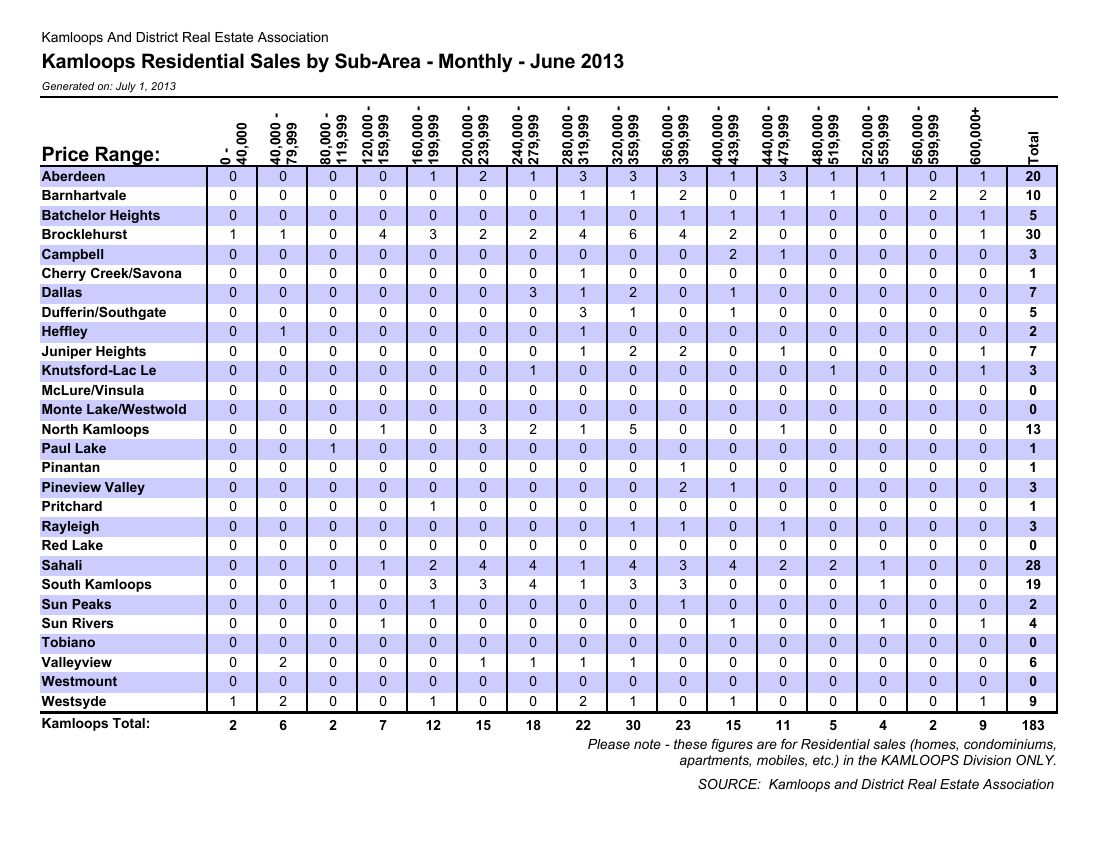

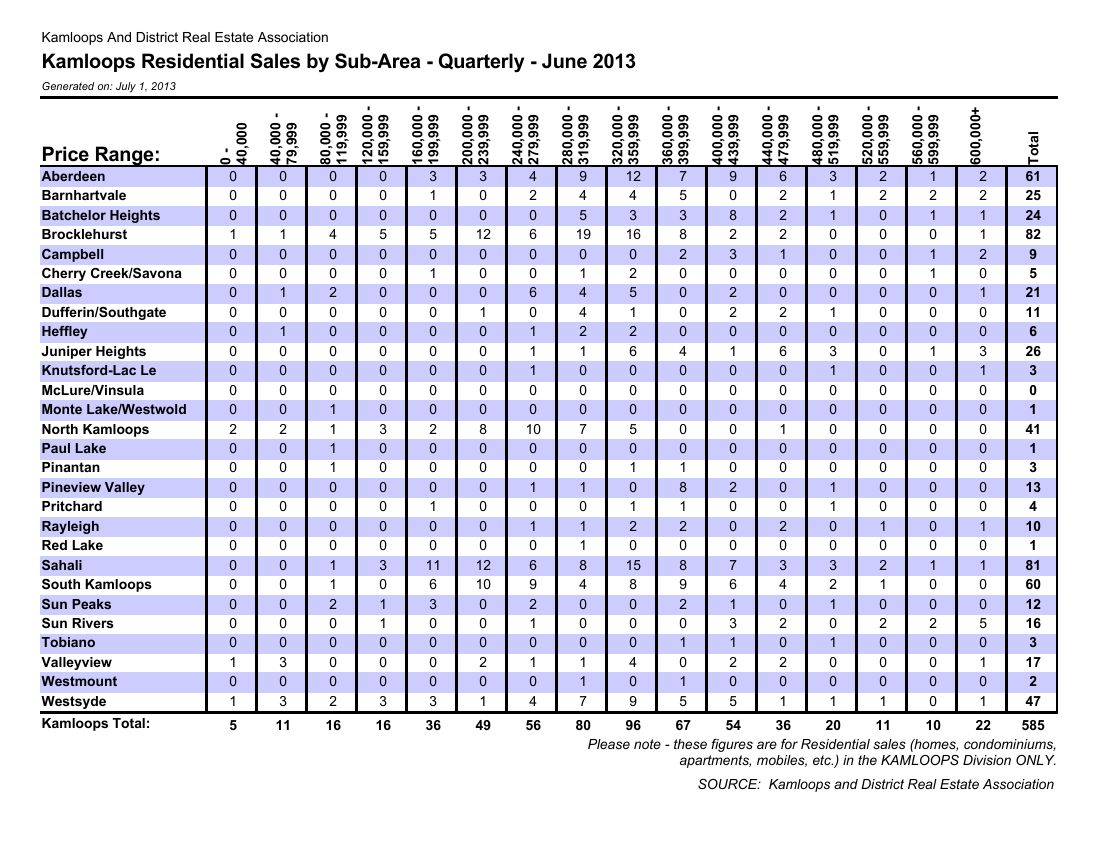

“On the resale side, prices have been pretty stable in Kamloops for the last year or two,” he said.