BC Home Sales Forecast to Rise Through 2016, BCREA 2015 First Quarter Housing Forecast Update

Vancouver, BC – February 11, 2015. The British Columbia Real Estate Association (BCREA) released its 2015 First Quarter Housing Forecast Update today.

Click to enlarge

“Stronger economic conditions both at home and abroad combined with favourable interest rates and population growth are expected to bolster housing demand over the next two years,” said Cameron Muir, BCREA Chief Economist. “After a year in which housing demand ratcheted higher across the province, the retrenchment of oil prices is expected to attenuate housing demand in some regions while bolstering it in others.”

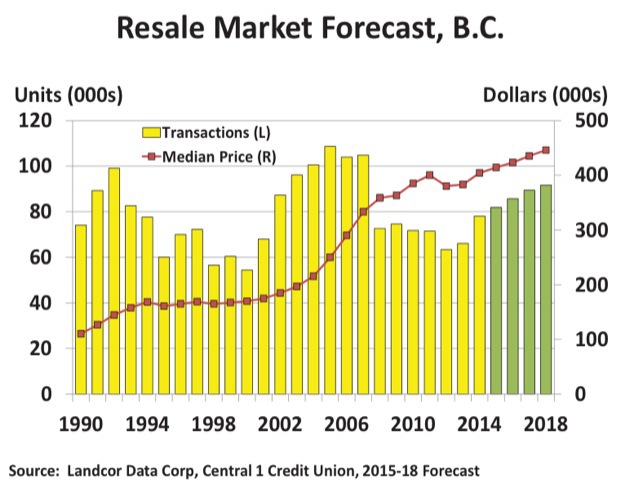

Multiple Listing Service® (MLS®) residential sales in British Columbia are forecast to rise 2.4 per cent to 86,050 units this year and a further 3.9 per cent to 89,400 units in 2016. The ten-year average is 82,100 unit sales. A record 106,300 MLS® residential sales were recorded in 2005.

The average MLS® residential sales price is forecast to rise 4.5 per cent to $594,000 this year, with most of the upward pressure being exhibited on the South Coast. Elevated consumer demand is expected to be partially offset by resale inventories and additions to the housing stock in 2016. As a result, the average MLS® residential sales price is forecast to increase by 2.4 per cent to $608,500 next year.

To view the full BCREA Housing Forecast Update, click here.

Residential construction is booming in the City of Kamloops in 2015 as 28 new residential unit permits were approved in January.

Residential construction is booming in the City of Kamloops in 2015 as 28 new residential unit permits were approved in January.