This article appeared on the Business News Network on January 14th, 2016 and was written by Fergal Smith of Reuters.

Bank of Canada interest rate cut speculation intensified on Tuesday as crude oil prices and the Canadian dollar both weakened to 12-year lows, with traders pricing in a full 25-basis-point easing by mid year.

The Canadian central bank cut rates twice in 2015 as an oil price shock drove the economy into recession in the first half of the year, but has been sidelined since July.

“People are calling for the Bank of Canada to cut rates at the next meeting,” said David Bradley, director of foreign exchange trading at Scotiabank.

The implied probability of a Bank of Canada rate cut at next week’s interest rate announcement has climbed from 22 percent after a speech by Governor Stephen Poloz last week to more than 30 percent, while the market has nearly fully discounted a rate cut in May.

The prospect of easing helped drive the yield on the Canadian government’s two-year bond to a four-month low.

Even so, “the market is underpricing the probability of a rate cut next week,” said Andrew Kelvin, senior rates strategist at TD Securities.

A Jan. 7 speech by Poloz had left investors doubtful he would cut Canada’s benchmark rate this month.

However, the central bank’s quarterly Business Outlook Survey has since found that business sentiment has deteriorated, while investment and hiring intentions have fallen to their lowest levels since 2009.

“It’s clearly going to be a very close call for the Bank of Canada given the financial turmoil we have seen,” said Kelvin.

U.S. crude oil prices have fallen an additional 8 percent this week, dipping below US$30 a barrel. Moreover, Western Canada Select, a blend produced by Canadian oil companies, trades at a greater than $14 discount to U.S. crude oil prices.

“We know falling oil prices have preceded both the last two cuts from the Bank (of Canada),” said Kelvin.

The central bank assumed a $45 price for U.S. crude oil prices when making its latest forecasts for the economy in October.

Speaking on Tuesday, Canadian Finance Minister Bill Morneau acknowledged that the public is concerned about the economy, but declined to indicate whether the government will stick to its budget deficit pledge or boost spending.

“We will be working in our budget to make sure that our initiatives help to grow the economy. We think the initiatives we already outlined are the appropriate initiatives to make a difference,” he said.

This article appeared on CBC.ca on the 29th of May 2015.

Canadians are showing a strong ability to manage their debts even as housing prices rise, with arrears on CMHC mortgages at a low 0.34 per cent for the first quarter of this year, according to new figures from the federal housing agency.

That means there were 9,572 Canada Mortgage and Housing Corp.-insured mortgages in arrears in the quarter, while it insures a total of 2.8 million mortgages. It had to pay just 588 claims.

The gross debt service ratio for Canadian homeowners – the percentage of housing costs to gross monthly income – sits at 26 per cent for the three months ended March 31.

That’s almost the same as in the first quarter of 2014, but up slightly from 25 per cent in 2013.

The ratios are highest in Alberta, British Columbia and Ontario, where housing prices have been rising rapidly. New homeowners in those provinces are also more likely to need a CMHC mortgage, which is necessary when buyers do not have a 20 per cent down payment.

However, a small proportion of CMHC-insured homeowners – 12.1 per cent – have a gross debt service ratio of more than 35 per cent, meaning more than a third of their monthly income goes to housing costs.

Another 21 per cent of CHMC-insured mortgage holders are juggling housing costs of 30 to 35 per cent of their gross income.

As housing costs rise, more than a quarter of the mortgages insured by CMHC are for over $400,000.

However, the average insured loan amount was $238,630.

In its annual report the federal agency predicts today’s low interest rates will continue to stimulate demand for housing.

It expects mortgage rates will not rise in Canada before the end of 2015.

The report comes after CEO Evan Siddall said CMHC’s share of the mortgage market had dropped from about 90 per cent of new mortgages to about half of new mortgages.

Ottawa had encouraged the agency to reduce exposure to mortgage defaults for the Canadian taxpayer, saying it wanted private insurers to take over the risk.

In its annual report, CMHC said it insured mortgages worth $543 billion in 2014, down 4.1 per cent from 2012, and below the legal limit of $600 billion.

OTTAWA, ONTARIO–(Marketwired – April 2, 2015) – As a result of its annual review of its insurance products and capital requirements, CMHC is increasing its homeowner mortgage loan insurance premiums for homebuyers with less than a 10% down payment. Effective June 1, 2015, the mortgage loan insurance premiums for homebuyers with less than a 10% down payment will increase by approximately 15%.

For the average Canadian homebuyer who has less than a 10% down payment, the higher premium will result in an increase of approximately $5 to their monthly mortgage payment. This is not expected to have a material impact on housing markets.

Premiums for homebuyers with a down payment of 10% or more and for CMHC’s portfolio insurance and multi-unit insurance products remain unchanged. The changes do not apply to mortgages currently insured by CMHC.

“CMHC completed a detailed review of its mortgage loan insurance premiums and examined the performance of the various sub-segments of its portfolio,” said Steven Mennill, Senior Vice-President, Insurance. “The premium increase for homebuyers with less than a 10% down payment reflects CMHC’s target capital requirements which were increased in mid-2014.”

CMHC is mandated to operate its mortgage loan insurance business on a commercial basis. The premiums and fees it collects and the investment income it earns cover related claims and other expenses while providing a reasonable rate of return on its capital holding target.

CMHC contributes to the stability of Canada’s housing finance system, including housing markets, by providing qualified Canadians in all parts of the country with access to a range of housing finance options in both good and bad economic times.

Effective June 1st, CMHC Purchase (owner occupied 1 – 4 unit) mortgage loan insurance premiums will be:

Loan-to-Value Ratio

Standard Premium (Current)

Standard Premium (Effective June 1st, 2015)

Up to and including 65%

0.60%

0.60%

Up to and including 75%

0.75%

0.75%

Up to and including 80%

1.25%

1.25%

Up to and including 85%

1.80%

1.80%

Up to and including 90%

2.40%

2.40%

Up to and including 95%

3.15%

3.60%

90.01% to 95% – Non-Traditional Down Payment

3.35%

3.85%

CMHC reviews its premiums on an annual basis and will announce decisions on premiums following this review.

Canada Mortgage and Housing Corporation (CMHC) has been Canada’s authority on housing for more than 65 years.

CMHC helps Canadians meet their housing needs. As Canada’s authority on housing, we contribute to the stability of the housing market and financial system, provide support for Canadians in housing need, and offer objective housing research and advice to Canadian governments, consumers and the housing industry. Prudent risk management, strong corporate governance and transparency are cornerstones of our operations.

For additional highlights please see the backgrounder info below and visit CMHC’s key fact sheet.

BACKGROUNDER

Mortgage loan insurance helps protect lenders against mortgage default and enables consumers to purchase homes with a minimum down payment of 5% with interest rates comparable to those with a 20% down payment. Mortgage loan insurance is typically required by lenders when homebuyers make a down payment of less than 20% of the purchase price.

CMHC’s new premium rates will be effective for new mortgage loan insurance requests submitted on or after June 1, 2015. The current mortgage loan insurance premiums will apply for applications submitted to CMHC prior to June 1, 2015, regardless of the closing date. As is normal practice, complete borrower and property details must be submitted to CMHC when requesting mortgage loan insurance.

The increase applies to mortgage loan insurance premiums for residential housing of 1 and 2 units for homebuyers with less than a 10% down payment.

CMHC mortgage loan insurance premium is calculated as a percentage of the loan based on the loan-to-value ratio. The premium can be paid in a single lump sum but more frequently is added to the mortgage principal and amortized over the life of the mortgage as part of regular mortgage payments.

CMHC reviews its premiums on an annual basis and has adjusted them several times since being commercialized in 1998. Adjustments have included both increases and decreases to the premiums.

CMHC’s capital holdings reduce Canadian taxpayers’ exposure to the housing market and contribute to the long term stability of the financial system. In August 2014, CMHC increased its capital holding target from 200% to 220% of the minimum OSFI requirements.

In 2014, the average CMHC insured loan at 95% loan-to-value was $252,530. Based on this figure, the higher premium will result in an increase of approximately $5 to the monthly mortgage payment for the average Canadian homebuyer. This is not expected to have a material impact on housing markets.

Genworth Canada To Increase Mortgage Insurance Premium Rates For Some Customers

(RTTNews.com) – Genworth MI Canada (MIC.TO) Monday said that effective June 1, it would increase its mortgage insurance premium rates for homebuyers with less than a 10 percent down payment by around 15 percent.

A typical first-time homebuyer taking out a 95 percent loan-to-value mortgage of $300 000 will see an increase of approximately $6 in their monthly mortgage payment, based on a 2.79 per cent interest rate and 25-year amortization period.

“This new pricing is reflective of higher capital requirements and supports the long-term health of Canada’s housing finance system,” said Stuart Levings, President and CEO of Genworth Canada.

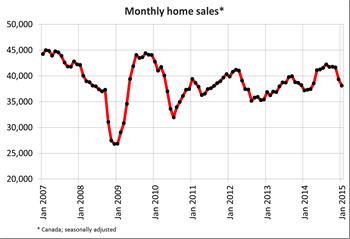

Ottawa, ON, February 17, 2015 – According to statistics released today by The Canadian Real Estate Association (CREA), national home sales activity was down on a month-over-month basis in January 2015.

Highlights:

– National home sales fell 3.1% from December to January.

– Actual (not seasonally adjusted) activity stood 2.0% below January 2014 levels.

– The number of newly listed homes rose 0.7% from December to January.

– The Canadian housing market remains balanced.

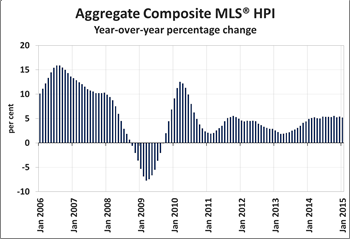

– The MLS® Home Price Index (HPI) rose 5.17% year-over-year in January.

– The national average sale price rose 3.1% on a year-over-year basis in January.

The number of home sales processed through the MLS® Systems of Canadian real estate Boards and Associations fell 3.1 per cent in January 2015 compared to December 2014.

January sales were down from the previous month in about 60 per cent of all local housing markets. On a provincial basis, the monthly decline largely reflected fewer sales in Alberta and Saskatchewan.

Click to enlarge

“As expected, consumer confidence in the Prairies has declined and moved a number of potential homebuyers to the sidelines as a result,” said CREA President Beth Crosbie. “By contrast, housing market trends in the Maritimes are continuing to improve, which underscores the fact that all real estate is local. Nobody knows this better than your local REALTOR®, who remains your best source for information about the housing market where you currently live or might like to in the future.”

Actual (not seasonally adjusted) activity in January stood two per cent below levels reported in the same month last year, marking the first year-over-year decline since April 2014.

“Comparing sales activity for January this year to sales one year earlier, there was a fairly even split between the number of markets where sales were up versus the number of markets where sales were down,” said Gregory Klump, CREA’s Chief Economist. “The decline in national sales largely reflects weakened activity in Calgary and Edmonton. If these two markets are removed from national totals, combined sales activity remained 1.9 per cent above year-ago levels.”

The number of newly listed homes rose 0.7 per cent in January compared to December. New supply climbed higher in just over half of all local markets, led by Edmonton and Greater Toronto. By contrast, Greater Vancouver, Calgary, and Regina posted the largest monthly declines in new listings.

The national sales-to-new listings ratio was 49.7 per cent in January, marking the first time this measure of market balance has dipped below 50 per cent since December 2012.

Click to enlarge

A sales-to-new listings ratio between 40 and 60 per cent is generally consistent with balanced housing market conditions, with readings above and below this range indicating sellers’ and buyers’ markets, respectively. The ratio was within this range in more than half of all local markets in January.

The number of months of inventory is another important measure of the balance between housing supply and demand. It represents the number of months it would take to completely liquidate current inventories at the current rate of sales activity.

There were 6.5 months of inventory nationally at the end of January 2015, its highest reading since April 2013. As with the sales-to-new listings ratio, the reading for the number of months of inventory still indicates that the national market remains balanced.

The Aggregate Composite MLS® HPI rose by 5.17 per cent on a year-over-year basis in January. This continues the trend, in place throughout 2014, where year-over-year price gains held steady between five and five-and-a-half per cent.

Year-over-year price growth held steady in January for one-storey single family homes and decelerated for other Aggregate Benchmark housing types tracked by the index.

Two-storey single family homes continued to post the biggest year-over-year price gains (+6.57 per cent), followed closely by townhouse/row units (+5.00 per cent) and one-storey single family homes (+4.61 per cent). Price growth remained comparatively more modest for apartment units (+3.11 per cent).

Price gains varied among housing markets tracked by the index. As in recent months, Calgary (+7.76 per cent), Greater Toronto (+7.47 per cent), and Greater Vancouver (+5.53 per cent) continued to post the biggest year-over-year increases.

That said, while prices in Greater Vancouver and Greater Toronto continue to trend higher, the trend for prices in Calgary has been fairly stable since last summer while year-over-year gains continue to shrink.

In other markets from West to East, prices were up on a year-over-year basis in the Fraser Valley, Victoria, and Vancouver Island, while remaining stable in Saskatoon, Ottawa, and Greater Montreal. By contrast, prices declined on a year-over-year basis in Regina and Greater Moncton.

The MLS® Home Price Index (MLS® HPI) provides a better gauge of price trends than is possible using averages because it is not affected by changes in the mix of sales activity the way that average price is.

The actual (not seasonally adjusted) national average price for homes sold in January 2015 was $401,143. This represents an increase of 3.1 per cent year-over-year and the smallest increase since April 2013.

The national average home price remains skewed by sales activity in Greater Vancouver and Greater Toronto, which are among Canada’s most active and expensive housing markets. Excluding these two markets from the calculation, the average price is a relatively more modest $312,280, which represents a year-over-year decline of three tenths of one per cent.

These two charts came from the Hufington Post on February 17th, 2015.

This article appeared on the Business News Network on January 14th, 2016 and was written by Fergal Smith of Reuters.

This article appeared on the Business News Network on January 14th, 2016 and was written by Fergal Smith of Reuters.