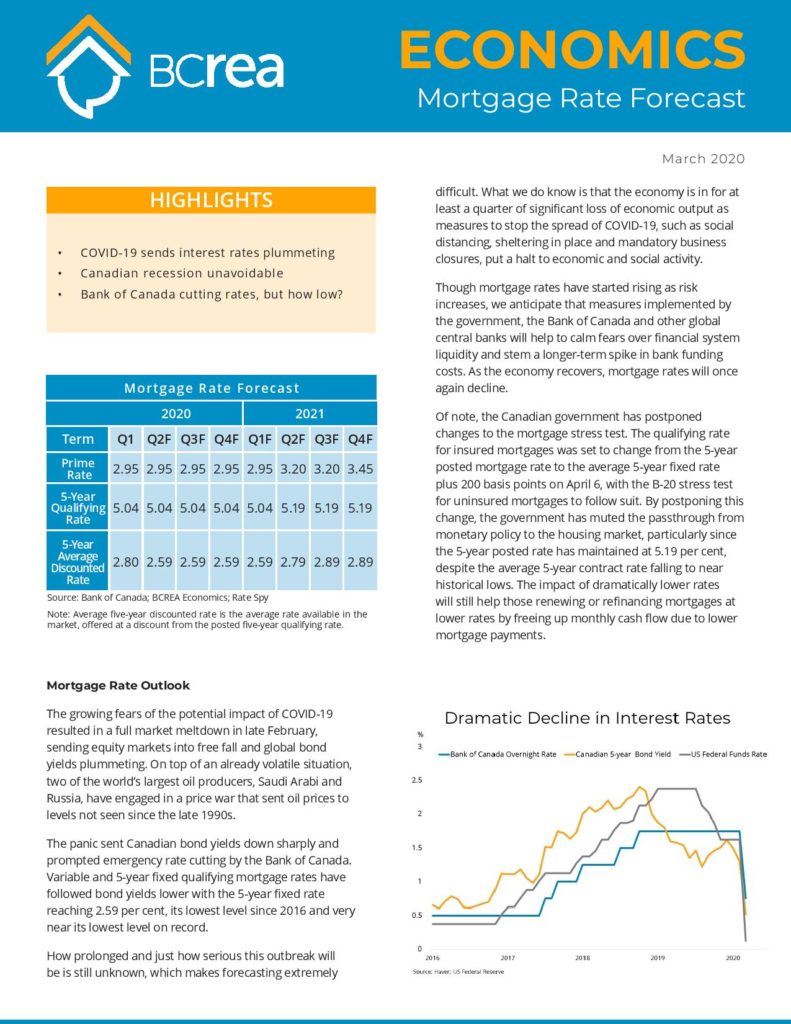

BCREA released it’s latest mortgage rate outlook. Read below and link to full report is included below.

The average Canadian 5-year fixed rate has fallen to under 2 per cent, the result of a rapid and overwhelming policy response from the Bank of Canada to the COVID-19 pandemic. The Bank swiftly brought its overnight rate to its effective lower bound of 25 basis points and used the impressive scope of its balance sheet to counteract a nascent rise in credit spreads. Those measures, and those of its global counterparts, helped to forestall a potential repeat of the credit crisis that shocked the global economy over a decade ago.

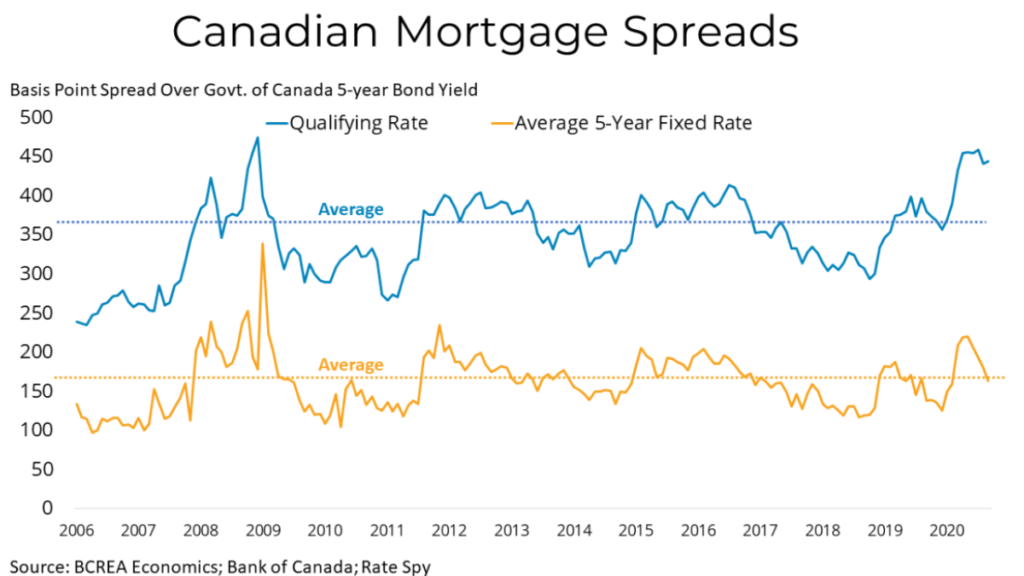

The Bank’s foray into quantitative easing (QE), or the purchasing of bonds across the yield curve of short-to-long term maturities, and an injection of liquidity into the mortgage market have resulted in record-low Canadian mortgage rates. The average 5-year fixed rate now sits below 2 per cent and is just 165 basis points over the 5-year government bond yield, essentially in line with the long-term average.

While the average 5-year rate has come down considerably, the qualifying rate remains stubbornly high at 4.79 per cent. That rate has become notoriously divorced from its underlying benchmark in recent years and now sits at a spread of close to 450 basis points over the 5-year bond yield, or about 100 basis points higher.

With the Bank of Canada eschewing negative interest rates and providing forward guidance that it has no plans to raise its policy rate until slack in the economy is absorbed, there is not much on the horizon that may move mortgage rates one way or the other. We expect a mild rise in rates as the Bank slows and eventually ends its QE, perhaps by the end of 2021. Studies show QE lowers long-term interest rates by 10-25 basis points, so we can anticipate a similar magnitude rise in 5-year rates when QE ends.

BCREA just released it’s Mortgage Rate Forecast for March and the year of 2020. With the COVID-19 mortgage rates have dropped. The Bank of Canada recently cut the rate again however says it is at a point where it can’t go lower. It is looking like a Canadian recession is unavoidable however it all depends on how long the pandemic related regulations go on for. This is a large factor that prevents accurate predictions since we have not seen an event of this magnitude in decades.

The Canadian government has postponed changes to the mortgage stress test due to the current events. This will help those renewing or refinancing their mortgages which will free up monthly cash flow due to the lower payments.

Economic growth in Canada was slowed at the end of 2019 due to the rail blockades and now COVID-19. The economy is also dealing with plummeting oil prices, a sharp decline in retail sales, tourism and other consumer related businesses.

It is expected that if we have a strong recovery in the second half of 2020 the Bank of Canada will likely maintain it’s policy rate at 0.25% for the rest of the year.

Click here to download the full PDF version of this report.

Click here to visit to BCREA’s website. To view other statistics for the Kamloops and BC real estate market click here.

• Rising rates and tighter mortgage regulations in 2018

• Canadian economy slowing

• Bank of Canada waiting on higher inflation

Mortgage Rate Outlook

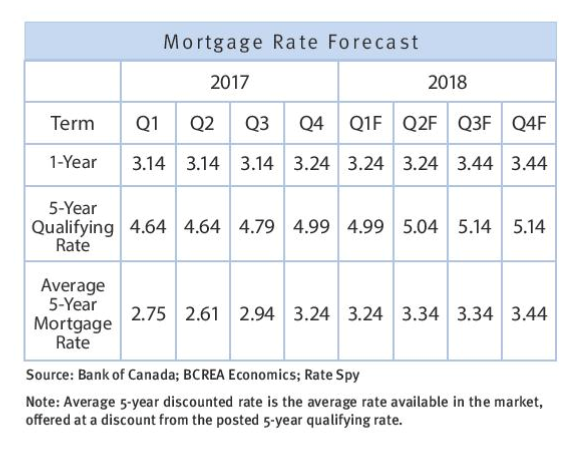

Canadian mortgage rates rose substantially in 2017 and are forecast to rise further in 2018. After beginning the year at or near historical lows for both the qualifying rate as well as 5-year contract rates, an acceleration of economic growth prompted a shift at the Bank of Canada and a withdrawal of stimulus implemented to help the economy absorb the oil-shock of 2015.

After the hawkish turn by the Bank of Canada, the Canadian 5-year bond yield, the key benchmark for the mortgage qualifying rate, seemed set on a higher trajectory before a slowing economy and the tepid inflation resulted in markets reassessing the likelihood of further rate hikes. The 5-year mortgage qualifying rate now sits at a three-year high of 4.99 per cent, while most lenders offer a discounted rate of 3.24 per cent. Our baseline forecast for

2018 is for those rates to increase to 5.15 per cent and 3.44 per cent, respectively.

One complicating factor will be the impact of new mortgage regulations, which require borrowers with more than 20 per cent equity to qualify at a rate at least as high as the 5-year posted mortgage rate. This will erode purchasing power by as much as 20 per cent, and will likely cause some prospective buyers to delay home purchases. Since non-federally regulated lenders such as credit unions do not need to comply with those regulations, large bank lenders could hold off on raising mortgage qualifying rates to remain competitive.

Economic Outlook

In the four quarters from the second half of 2016 to the first half of 2017, the Canadian economy grew at an average quarterly rate of 3.6 per cent, posting more than 4 per cent

growth in the second quarter of 2017. However, in the third quarter, growth slowed to just 1.7 per cent.

Despite a second-half slowdown, the Canadian economy still saw a surge in employment in October and November and will post annual real GDP growth of over 3 per cent in 2017, making it the envy of most advanced economies around the world.

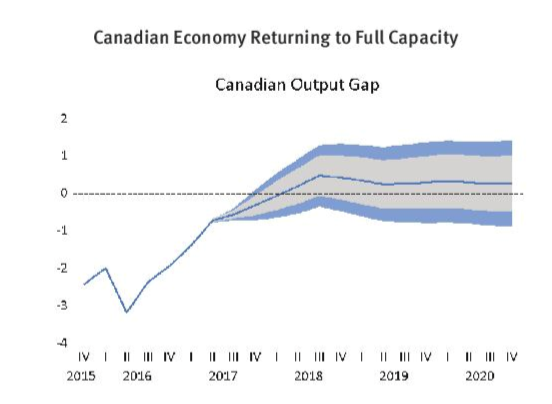

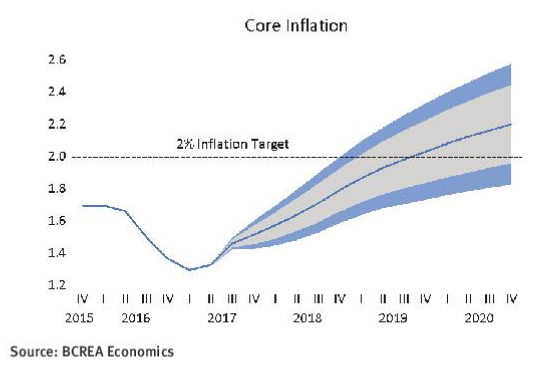

We do not expect that performance to be repeated in 2018, as the effect of higher interest rates and trade disputes present a drag on growth. Those factors are forecast to slow the overall Canadian economy to a still above-trend 2.2 per cent growth next year. As relatively strong growth continues to erode slack in the economy, inflation should return to its 2 per cent target by the end of next year.

Interest Rate Outlook

Despite strong economic growth, Canadian inflation remains subdued. The argument for a more hawkish approach from the Bank of Canada relies on two factors.

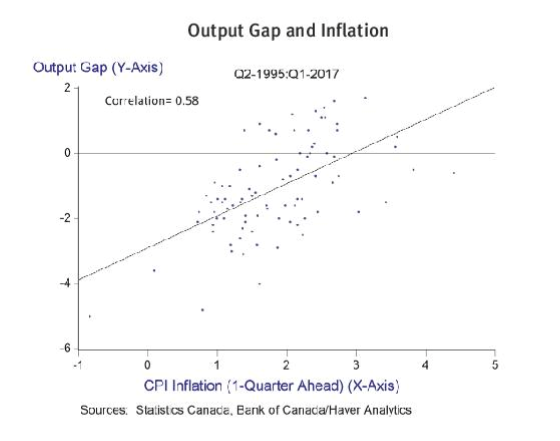

Firstly, that the elimination of unused capacity in the economy, generally referred to as the output gap, is inflationary. Therefore, an economy operating at or above capacity, as the Canadian economy is projected to do, should see rising price pressure. That view is supported by statistical evidence, though inflation has been well anchored due to the success of inflation targeting.

Secondly, the Bank’s framework for monetary policy is built upon setting interest rates at a “neutral” level to stabilize consumer price inflation around the Bank’s 2 per cent target. Since the Bank’s policy rate is currently 200 basis points below its estimate of “neutral,” there is an upward tilt to the Bank’s bias. That is, all else equal, the Bank would prefer to see interest rates “normalize” to a higher level over the medium term.

Still, there are significant risks to the downside for the Canadian economy over the next year. Elevated household debt presents a challenging tight-rope for monetary policy, as rates rising too quickly could have substantial and widespread consequences. Moreover, forthcoming restrictions on mortgage qualifying will already have a dampening impact on housing demand, which should also factor into the Bank’s thinking on monetary policy.

Weighing those risks against expectations of a closing output gap and inflation slowly moving toward 2 per cent over the next year, the Bank may still find just enough

reason to raise the its target rate once or twice in 2018.

This article appeared on the CBC News website on January 20th, 2016 and was written by Sheena Goodyear.

Despite a topsy-turvy mortgage landscape that has seen rates go up unexpectedly, don’t expect your monthly payments to skyrocket any time soon, economists say.

“I think that mortgage rates will remain relatively stable,” CIBC deputy chief economist Benamin Tal told CBC News. “I just don’t see anything that will send them up.”

Mortgage rates have been creeping up over the last few months— a fact that may have many homeowners scratching their heads.

Usually a turbulent economy, like the one Canada is currently facing, with oil below $30 US a barrel and the loonie lower than 70 cents US, would be accompanied by a drop in mortgage costs, especially fixed rates.

That’s because fixed mortgages are tied directly to government bond yields, which are at an all-time low as risk-wary investors steer clear of the stock market.

Still, all the major banks have announced mortgage-rate increases since December.

CIBC increased its three-year fixed rate by 10 basis points to 2.59 per cent. RBC upped its special offer on a five-year fixed mortgage by one-tenth of a point to 3.04 per cent. TD Bank increased its one-year and four-year closed special rates by one-tenth of a point each. Scotiabank increased its variable rate by 10 basis points.

Government regulations and global forces

Robert McLister, a mortgage planner at intelliMortgage and the founder of RateSpy.com, told Canadian Press the hikes stem partly from new government regulations designed to reduce risk in the country’s housing industry, including plans to force the banks to have more money set aside in case the mortgage loans on their books go bad.

“It’s going to be more expensive for banks to hold mortgages,” McLister said. “They have to put aside more capital and when you put aside more capital, then you can’t do other things with it. And that costs you money, so that gets baked into pricing.”

But it’s more complicated than that, said Tal. In order to understand Canadian mortgage rates, you have to look at the global picture.

“Given the uncertainty and given the fact that risk profiles are rising globally, I think that the Canadian banks have to pay more to fund themselves,” he said.

Still, there’s no reason for homeowners and would-be homeowners to fret over modest hikes to already low rates, John Andrew, a real-estate professor from Queen’s University in Kingston, Ont., told CBC News.

“I think the rise we’ve seen in mortgage rates isn’t really very significant,” he said.

Bank of Canada holds key rate steady

Meanwhile, the prime rate — the interest rate commercial banks charge their most credit-worthy customers — is unlikely to change substantially any time soon after the Bank of Canada announced Wednesday it would leave its benchmark overnight rate unchanged at 0.5 per cent.

Changes to the overnight rate — the interest rate at which big banks borrow and lend — have traditionally had major implications for Canadian mortgages, as the big commercial banks would follow in lockstep with changes to their prime rate.

But even if the Bank of Canada had announced a rate change on Wednesday, the impact on mortgages likely would have been minimal. The central bank’s power to influence the housing market has dwindled in recent years, economists say.

When the Bank of Canada slashed the overnight rate by 0.25 per cent a year ago, commercial banks only cut their prime rate by 0.15 per cent.

“That’s maybe something the [Bank of Canada] should look at, because the ability of the bank to really impact market rates and activity is very limited,” Tal said.

Rates will go up eventually

Despite the steady forecast for the next year or two, Andrew advises new homeowners or those looking to renew their mortgages to choose a fixed, or locked in, rate with regular monthly payments that aren’t tied to the prime.

“I’m a little gun-shy about variable-rate mortgages, just because you’re in a period where mortgage rates are so low and there isn’t a widespread expectation in the market that they’re going to rise dramatically,” he said.

“I’m a big one for certainty, and I think the big uncertainty is rising rates. We know they’re going to rise — we just don’t know when and we don’t know by how much. So do you want to get into a variable situation where you’ve got no control over that?”

Marcus Tzaferis, a mortgage broker with MorCan Direct, disagrees. There are good deals on variable-rate mortgages right now, he said, especially from non-bank lenders that won’t penalize you if decide to lock in.

“I’ve been doing this now for about 15 years — nothing happens all that quickly. This tool of inciting some fear that rates are going to go up — it almost works in the banks’ favour. The banks make more money on the fixed rate,” he said. “I don’t think we’re going to see rates increase any time soon.”

Tal said when it comes to fixed versus variable, it all comes down to the individual. There’s no one-size-fits-all for mortgages. But, he warned, the pendulum will eventually swing back, so it’s best to plan ahead.

“If you’re buying right now, it’s very, very likely that five years from now, when you renew, rates will be notably higher,” he said. “If you cannot finance your mortgage at rates that are one to two per cent higher, then you have to think twice about the type of house that you want to buy.”

Despite a topsy-turvy mortgage landscape that has seen rates go up unexpectedly, don’t expect your monthly payments to skyrocket any time soon, economists say.

Despite a topsy-turvy mortgage landscape that has seen rates go up unexpectedly, don’t expect your monthly payments to skyrocket any time soon, economists say.